For VAT purposes, supplies are divided into supplies of goods and supply of services. Different VAT location rules apply depending on whether the transaction is a supply of goods or supply of service. The question of who is liable for VAT (the supplier or the recipient) for a specific service also depends on the correct classification. Correct classification is essential, particularly in cross-border situations. Otherwise, there is a risk of charging the wrong VAT. For the service provider, this means that they may even owe VAT twice (once the VAT incurred by law and once the VAT invoiced ). For the recipient of the service, this means that they are not entitled to deduct input VAT from the incorrectly invoiced VAT amount. If they pay the VAT to the service provider, they can only reclaim it from them under civil law. If something goes wrong, losses of more than 50% of turnover are not uncommon in practice.

Principle of uniformity of performance

For VAT purposes, every supply of goods and every supply of service must be considered an independent transaction. Nevertheless, at least within the EU, the principle of uniformity of a transaction applies. A single economic transaction may not be artificially split up (section 3.10 (3) German VAT Circular). However, the prerequisite for a single service instead of several independent services is always that the activities are performed by the same taxable person (section 3.10 (4) German VAT Circular).

The assessment of whether the supplies are to be regarded independently or as a single coherent transaction is made from the perspective of the recipient of the transaction. Whether the single transaction is to be classified as a supply (in the form of a supply of goods/ supply of goods incl. installation/assembly or work delivery) or as supply of service (in the form of a supply of a work performance) must be determined in accordance with the law of the respective Member State. This is essential, especially where both materials are supplied and work is performed. This is because different legal standards have developed in the individual Member States for distinguishing between supplies of goods and upply of services .

Types of supplies of goods

A supply of goods is deemed to have taken place when the power of disposal over an item is transferred (Section 3 (1) German VAT Act, Section 3.1 (1) German VAT Circular). Items within the meaning of Section 3 (1) German VAT Act are physical items, collections of items, and economic goods that are treated as physical items in commercial transactions.

If there is a supply of goods that must be assessed independently or if the transaction qualifies as a uniform transaction in the form of a supply of goods, the exact type of supply of goods must be determined in detail. This is because the VAT assessment of a supply of gods depends on when the power of disposal over the item owed was transferred to the recipient of the service. At this point in time, the transaction is deemed to have been performed. Taxation takes place at the place and time at which the supplier has done everything necessary (including any material and labor) to ensure that, from the recipient's point of view, the expected service has been provided in full. This condition can be met at the supplier's premises, at the customer's premises, at a third party's premises, or even en route to the customer (e.g., in the case of a contract manufacturer).

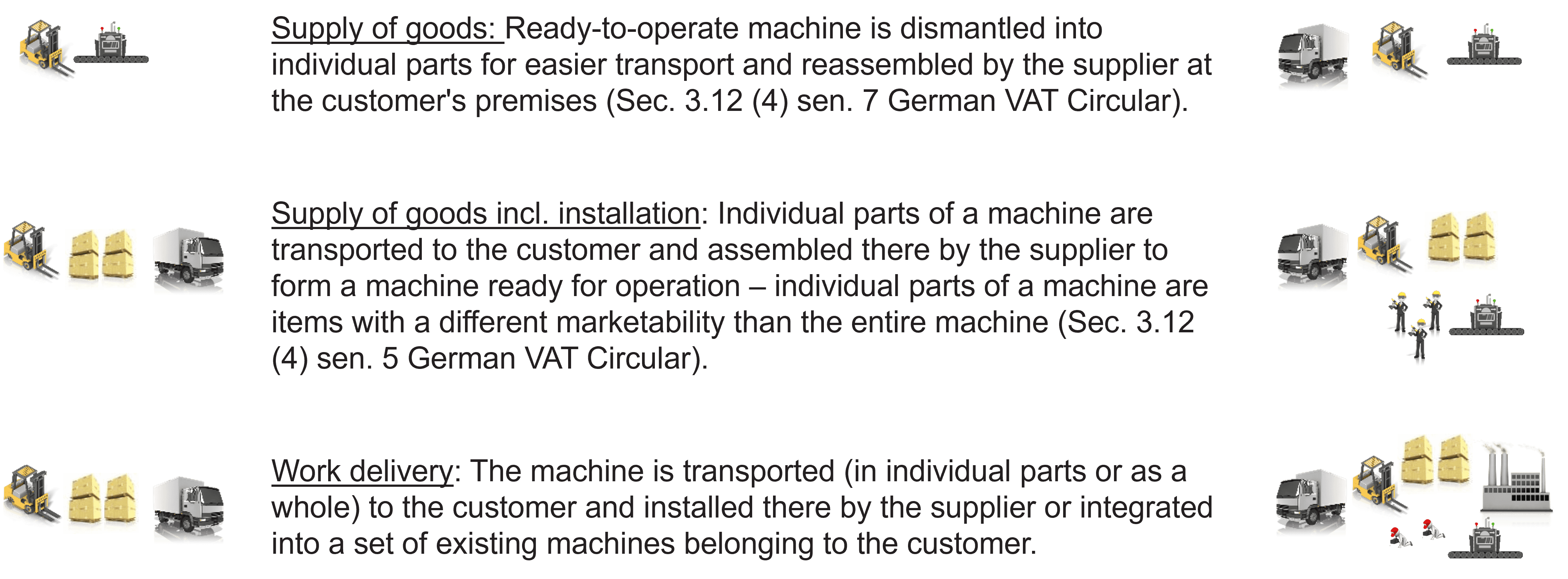

Supply of goods with transport

If the item is already finished at the time of transport to the particular customer, it is considered a supply of goods with transport. This transaction is taxable (outside of a chain transaction) at the place where the physical transport commences. Minor and insignificant work carried out on site shares the VAT treatment of the supply of gods with transport. The dismantling of the delivery item for logistical reasons is also irrelevant. According to Section 3.12 (4) German VAT Circular, the place of supply is determined in accordance with Section 3 (6) German VAT Act (supply with transport) if a machine that is ready for operation is dismantled into individual parts solely for the purpose of better and easier transport and is then reassembled by a the supplier at the place of destination. Ready-to-operate production at the supplier's premises usually includes a test run carried out there. A new test run carried out by the supplier after reassembly at the customer's premises is not detrimental.

If, for example, the item is transported across borders, the supplier can apply for a zero-rate for intra-Community supplies or export supplies.

Supply of goods including installation / assembly

A supply of goods with installation works and therefore a supply without transport, on the other hand, is assumed if more significant work still needs to be carried out at the customer's premises in order for the item to reach the condition required under the contract. There is no clear distinction between when work carried out on site constitutes a supply including installation or a work delivery (see below) and when it is no longer considered a supply of goods with transport. Above all, the VAT law of the respective country must be observed for cross-border activities. Each country, even within the EU, has developed different standards and points of reference for this issue.

If the item is transported to the project site in individual parts and is installed / assembled there, the item owed is first created at the customer's premises. According to Section 3.12 (4) German VAT Circular, it is no longer a supply of goods with transport if the individual parts of a machine are transported to the customer and installed / assembled there by the supplier to form a machine ready for operation. This is the case if, after the start of transport, the supply item undergoes treatment by the supplier that changes its marketability. The reason for this is that individual parts of a machine are to be regarded as items with a different marketability than the entire machine. It is irrelevant whether the installation / assembly costs are invoiced separately to the customer (see above: due to the principle of uniformity of a transaction, separate invoicing has no effect).

At this point, the individual parts of a machine that are transported to the customer are items with a different marketability than the entire machine. Since the item owed is already at the customer's premises at the time of transfer of power of disposal, this is a supply of goods with installation / assembly and therefore a supply of goods without transport that is taxable where the item reaches its contractually owed condition.

If the individual parts are transported across borders beforehand, an important exception within the EU must be observed. In principle, the cross-border transport of own goods within the EU triggers a registration obligation in the country of departure and the country of destination (intra-Community transfer of won goods[). However, if own goods are transported to the place of destination for the purpose of a supply including installation or assembly by the supplier or on his behalf, no intra-Community transfer of own goods is triggered (Article 17 (2) (b) VAT Directive / Section 1a (2) German VAT Act, Section 1a.2 (10) ff. German VAT Circular). However, this is subject to the condition that the goods are already attributable to the supplier's business at the start of transport. If items are purchased and transported directly to the customer, where they are installed or assembled, this constitutes an intra-Community acquisition by the purchaser in the country of destination, which in principle triggers a registration obligation there.

Since the supply including installation / assembly is a supply without transport, the transaction is not eligible for a zero-rate as an intra-Community supply or as an export supply.

Work delivery

Furthermore, individual countries, such as Germany and Austria, distinguish between supply including installation / assembly and a work delivery. This is again relevant to the question of a possible change of the person liable for VAT.

The term “work delivery” is defined in Germany in Section 3 (4) of the German VAT Act. According to Section 3 (4) sentences 1 and 2 German VAT Act, a work delivery exists if the taxable person has undertaken the processing or transformation of a foreign item and uses materials that he has procured himself. The transaction is to be regarded as a supply of goods if the materials are not merely ingredients or other incidental items. This also applies if the items are permanently attached to immovable property. When classifying the items used as main materials, the value ratio to the item provided is irrelevant. The only thing that matters is whether they are important to the recipient of the service (= main material) or are only used as aids to achieve the desired result (= incidental matter).

For a work delivery to exist, a further requirement must therefore be met. Work deliveries exist if the taxable person not only transfers the power of disposal over an item to the customer but also processes or transforms a third-party item. This has already been confirmed by the Federal Fiscal Court in its ruling of August 22, 2013 – V R 37/10. The tax authorities only adopted this view in the BMF letter dated October 1, 2020 (section 3.8 (1) sentence 1 German VAT Circular). As of 2025, the condition that a foreign item needs to be processed, is also clearly stated in the German VAT Act. The third-party item may also be immovable property (land/buildings/structures). In this case, the work delivery is generally provided in the form of a supply of construction work.

Most Member States do not distinguish between a supply including installation / assembly and work delivery, so that a distinction is not relevant there. The special feature in Germany and Austria, which do make a distinction, is that the VAT liability is only transferred in the case of work delivery if the supplier is a foreign taxable person. If only a supply of goods including installation / assembly is provided, the supplier remains liable for VAT, even if they are a foreign taxable person.

Since the supply of work is generally a supply of goods without transport, the transaction is not eligible for a zero-rate as an intra-Community supply or as an export supply . If own goods (see above under supply of goods including installation / assembly) are transported to the place of destination, this does not trigger intra-Community transfer of own goods (Art. 17 (2) (b) VAT Directive / § 1a (2) HS 2 German VAT Act, Section 1a.2 (10) ff. German VAT Circular).

Supply of Goods / Work Delivery / Supply of Goods incl. Installation /Supply of a Coherent Item:

Special case: Supply of a coherent item

However, even without any work being performed, the place of taxation may shift, for example if the subject of supply is a collection of items which belong together.

According to Section 3.1 (1) sentence 3 German VAT Circular, the combination of several independent items into a uniform whole which is economically regarded as a different tradable good than the sum of the individual items constitutes a collection of items. In its ruling of August 28, 1986, V R 18/77, the Federal Fiscal Court determined that the supply of a system is to be classified as the supply of a coherent of item consisting of installed / assembled purchased items if components of the system are intended for joint use and are coordinated in terms of their performance and the system was only created at the buyer's business premises.

A coherent item is ultimately the combination of several independent items into a uniform whole which is economically regarded as a different tradable good than the sum of the individual items. If, for example, individual machines are transported to the customer in a ready-to-operate state but are coordinated with each other as part of a system, so that the customer is interested in the supply of these individual machines as a whole, this constitutes a supply of a set of items (a coherent item). This supply is taxable at the place where the individual items are first physically brought together in their entirety. In practice, the supply of a coherent item set occurs, among other things, when a taxable person subcontracts the manufacture of various machines or systems to subcontractors, the machines arrive at the project site ready for operation when viewed independently, but a complete system consisting of the various machines is owed on site.

Supply of a work performance

If the taxable person does not use any own or self-procured materials in the performance of his services, or only uses materials that are considered ingredients or other incidental materials, this constitutes a supply of services in the form of a supply of a work performance (Section 3.8 (1), sentence 3 ff. German VAT Circular). According to Section 3.8 (1) sentence 4 German VAT Circular, ingredients and other ancillary items within the meaning of Section 3 (4) sentence 1 German VAT Act are to be understood as items which, when viewed as a whole from the perspective of the average observer, do not determine the nature of the transaction (see Federal Fiscal Court judgment of June 9, 2009, 12 H 100, German VAT Circular, this refers to items which, when viewed as a whole from the perspective of the average observer, do not determine the nature of the transaction (see BFH judgment of June 9, 2005 – V R 50/02, BStBl II 2006 p. 98). The place of taxation of the supply of a work performance is to be determined according to the rules for the supply of services. The work performance may also be provided in the form of supply of services in connection with immovable property (e.g., construction work) if the processed item is a component of immovable property.

Contact