Christmas parties, company cars, canteens, gifts for employees, etc. are nice gestures on the part of the employer, but they also have tax consequences. No other sector has so many special rules and simplifications for income tax purposes. However, the employee incentives mentioned above must always be taken into account for VAT purposes. In practice, income tax results and values are often also used for VAT purposes. However, caution should be exercised here: the special income tax regulations do not always apply to VAT!

VAT – basics of non-cash benefits for employees

Non-cash benefits provided by the employer to its staff can take many different forms and have many different reasons:

Non-cash benefits provided by the company to its staff for consideration or at a reduced rate on the basis of the employment relationship

Example:

Sale of company-owned products to employees at regular or reduced prices.

These are taxable supplies of goods or supplies of services for consideration in accordance with sec. 1 para. 1 no. 1 sentence 1 of the German VAT Act (UStG) and sec. 1.8 para. 1 sentence 4 of the German Administrative VAT Guidelines (UStAE). The taxable amount is determined in accordance with sec. 10 para. 1 UStG. Where applicable, the minimum taxable amount pursuant to sec. 10 para. 5 sentence 1 no. 2 UStG applies, sec. 1.8 para. 6 UStAE.

Non-cash benefits as remuneration for services rendered or to be rendered

Example:

Providing a company car to authorised signatories for private use in accordance with their employment contract as remuneration for services rendered.

The granting of the vehicle is to be classified as a taxable supply of services for consideration in accordance with sec. 1 para. 1 no. 1 sentence 1 UStG (supply similar to an exchange sec. 3 para. 12 sentence 2 UStG). The supply is therefore made for consideration, sec. 1.8 para. 1 sentence 1 UStAE. The taxable amount is determined in accordance with sec. 10 para. 2 sentence 2 UStG (in conjunction with sec. 10 para. 5 sentence 1 no. 2, sec. 4 UStG; sec. 1.8 para. 6 UStAE). Income tax values may be used, but not special regulations for electric and hybrid cars.

Non-cash benefits provided by the company to its employees for their private use, which are treated as supplies of goods or supplies of services for remuneration

Example:

The transport of employees from their homes to their workplace free of charge;

Excluded from this are: gifts and supplies that are mostly motivated by business interests.

Such non-cash benefits for private use are treated as supplies of goods or supplies of services for remuneration constitute taxable supplies of goods pursuant to sec. 3 para. 1b sentence 1 no. 2 UStG or taxable supplies of services pursuant to sec. 3 para. 9a nos. 1 and 2 UStG. However, as they are provided free of charge, they are fictitiously treated as transaction for consideration. Sec. 10 para. 4 UStG (sec. 1.8 para. 7 UStAE) must be used to determine the taxable amount.

Employees

According to sec. 3 para. 1b sentence 1 no. 2 UStG and sec. 3 para. 9a no. 1 and no. 2 UStG the term ‘personal’ includes employees and their relatives, pensioners, trainees and interns.

Income tax – basics non-cash benefits for employees

As a general rule, non-cash benefits that are provided mostly in the company's own interest do not constitute remuneration. They are not remuneration if they do not represent payment for the provision of labour, but are merely a necessary accompaniment to the operational objectives of the company.

Non-cash benefits that are not provided predominantly in the company's own interest, on the other hand, constitute wages. However, VAT exemptions under the German Income Tax Act (EStG) may apply here, e.g. the VAT exemption for tips (Sec. 3 no. 51 EStG) and job tickets (Sec. 3 no. 15 EStG).

Similarly, wages to which no VAT exemption applies may be subject to special valuation rules. Such special valuation must be carried out, for example, in the case of employee discounts pursuant to sec. 8 para. 3 of the German Income Tax Act with a discount allowance of €1,080 per year.

A consideration and examination must be carried out in each individual case on the basis of criteria developed by the Federal Fiscal Court (see, for example, Federal Fiscal Court, judgment of 24 September 2013 – VI R 8/11).

General valuation rule, sec. 8 para. 2 sentence 1 EstG

Appreciations, R 19.6 of the Income Tax Regulations (LStR)

Non-cash benefits do not constitute wages if they are gifts.

Non-cash benefits up to EUR 60;

Occasion: special personal event of the employee or a member of their householdBeverages and luxury foods at the place of work

Meals up to EUR 60 (on the occasion of and during exceptional work assignments)

For appreciations with a value not exceeding EUR 60, particular attention must be paid to proper documentation.

See VAT Newsletter 22/2015: VAT consequences of Wage Tax changes for company events and small gifts

Employees according to administrative guidelines

Employees are persons who are or were or will be employed or engaged in public or private service and who receive wages from this, a previous or future employment relationship. This also includes the legal successors of these persons, insofar as they receive wages from the previous employment relationship of their legal predecessor.

Temporary agency workers and employees of affiliated companies are generally employees, but their employer is usually the temporary employment agency or the affiliated company – not the user company. Shareholder-managing directors are also employees because of/for their services as managing directors, regardless of the size of their shareholding.

Gifts to employees

For income tax treatment, gifts to employees are not considered wages if they do not exceed a monthly exemption limit of EUR 50 – if the occasion is a special personal event, the value may not exceed EUR 60.

For VAT treatment, gifts given on the occasion of special personal events are not considered a supply carried out free of charge up to a value of EUR 60, and the employer is entitled to deduct input VAT. If this amount is exceeded and the supply carried out free of charge is already planned at the time of procurement of goods or services, the employer is not entitled to deduct input VAT on the purchase of the gift.

Vouchers

If a voucher is issued to an employee, the type of voucher must be determined for VAT purposes. Depending on the type of voucher, a distinction must be made between the issue and redemption of the voucher for VAT purposes.

Issue

Redemption

Single-purpose voucher

In the case of a single-purpose voucher, the issue is relevant for VAT treatment (sec. 3 para. 14 sentence 1 UStG): A fictitious supply in the amount of the voucher value is made between the seller and the employer. Consequently, the seller must pay VAT to the tax authority when the voucher is purchased by the employer.

The distinction between single-purpose and multi-purpose vouchers is crucial!

See

VAT Newsletter 20/2024: ECJ comments on definition of single-purpose vouchers and B2B voucher distribution

VAT Newsletter 10/2023: Federal Fiscal Court: voucher codes as single-purpose vouchers - doubts about the ‘known place of supply’

The purchase of the voucher (seller – employer) is not subject to income tax. The transfer to the employee constitutes a monetary benefit at the time of transfer. However, the voucher is not subject to income tax if the exemption limit of EUR 50 is not exceeded in the month of issue, sec. 8 para. 2, sentence 11 EStG. The redemption is also generally irrelevant for income tax treatment, unless the voucher is redeemed with the employer itself.

Other non-cash benefits in the month of issue must also be taken into account for the exemption limit. In addition, the Payment Services Oversight Act (ZAG) criteria must be met.

Multi-purpose voucher

If the voucher is a multi-purpose voucher, then only the redemption of the voucher by the employee is relevant for VAT purposes, sec. 3 para. 15 sentence 1 UStG. All previous transactions are irrelevant. The redemption of the multi-purpose voucher is offset by the supply made by the seller to the employee. The seller must then pay VAT to the tax authority when the voucher is redeemed.

For the purposes of income tax treatment of vouchers, the distinction between single-purpose and multi-purpose vouchers is irrelevant. The decisive factor here is always the date of issue to the employee.

Meals

Many companies pay meal allowances or maintain their own canteens. These are also relevant for both VAT and income tax treatment.

Company canteen

If employees are provided with meals in a company canteen, VAT is chargeable on the value of the meal and the amount of the employee's additional payment, sec. 1.8 para. 11 UStAE.

For income tax treatment, the employee's additional payment must be deducted from the value of the meal in order to determine the employee's monthly monetary benefit. For VAT treatment, the assessment is based on the individual case and may differ from the income tax assessment.

The value of the meal is generally based on the price paid for the meal. However, at least the official non-cash benefit value according to the Social Security Compensation Directive (SvEV) must be used.

For income tax treament, a flat-rate income tax of 25% may also be considered, pursuant to sec. 40 para. 2 no. 1 EStG.

Important: The canteen subsidy for an externally operated canteen is classified differently!

In practice, the external canteen operator invoices the employer for the discounted meals on a monthly basis. These so-called canteen subsidies are often the subject of VAT discussions. While the discount itself is to be treated as income tax as described above, the question arises as to whether the input VAT on the canteen subsidy can be deducted for VAT purposes. The tax authorities take the view that the employer cannot deduct input VAT from the canteen operator's invoice for the canteen subsidy. The jurisprudence classifies the canteen subsidy differently. It must be examined on a case-by-case basis whether the employer can claim input VAT on the canteen subsidy invoiced to it by the canteen operator.

Restaurant vouchers or meal vouchers

Restaurant vouchers can take various forms. They can be single-purpose or multi-purpose vouchers issued by the employer ‘in addition to wages’ or as part of a salary conversion scheme. The treatment for income tax and VAT purposes differs.

Business partners / Business dinners

If an employer invites business partners and employees to a meal as part of a project meeting or a business lunch, such expenses are entirely business-related. If all other requirements are met, input VAT can be claimed in full for these expenses. For income tax purposes, there is no monetary benefit insofar as the employee's participation is primarily in the interests of the business.

If the employer entertains the employee free of charge without a specific business reason, e.g. without the participation of a business partner, this constitutes a non-cash benefit for income tax purposes. The employer is not entitled to deduct input VAT.

Business occasions that make the catering appear to be predominantly in the interests of the business include, for example, inventories and unusual late work/project work, as regularly occurs in groups of companies during the annual financial statements.

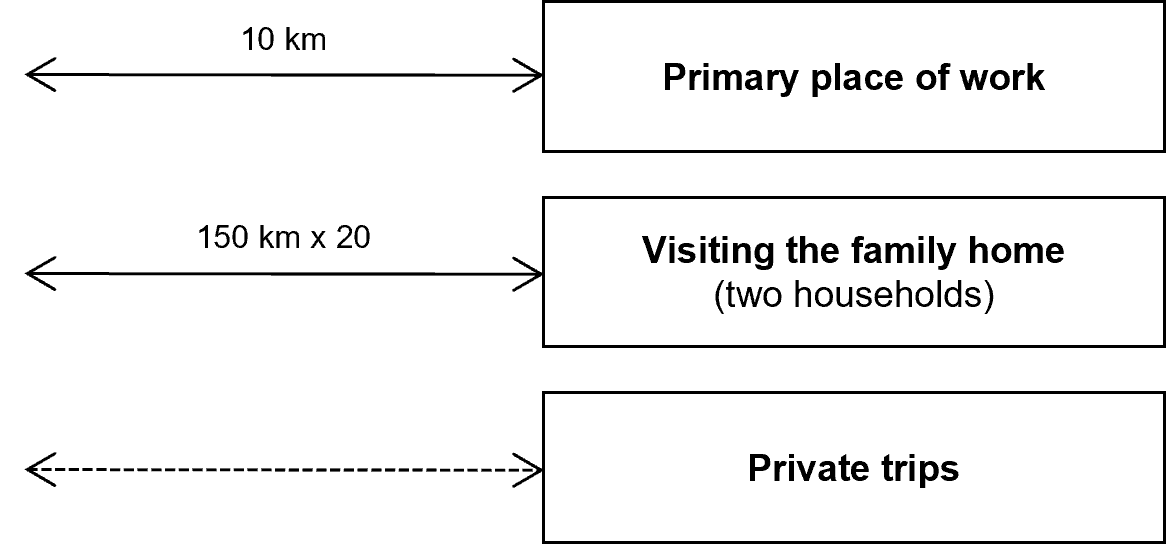

Providing company cars to employees

Example

An employee receives a hybrid electric company car. The gross value of the vehicle is EUR 30,000. He uses it for 15 trips of 10 km each way per month to his primary place of work. He also drives to visit his family every 2 to 3 weeks (approx. 20 trips per year; double household). The distance is 150 km. He also makes other private trips in between.

Income tax treatment

In a letter dated 3 March 2022, the Federal Ministry of Finance addressed the income tax treatment of the transfer of a motor vehicle to an employee. In principle, the employer has a choice of valuation methods:

Flat-rate method, sec. 8 para. 2 sentences 2, 3, 5 EStG and R 8.1 para. 9 no. 1 LStR:

- The taxable amount for this method is based on the gross list price, i.e. the manufacturer's recommended retail price including special registration at the time of initial registration.

- When determining the value in use, a distinction must be made between private trips, trips to the primary place of work and trips made due to double household management.

- Additional payments made by the employee must be deducted, as these reduce the monetary benefit. However, salary conversion does not constitute an additional payment.

- If the flat-rate value in use exceeds the total costs incurred by the employer for the motor vehicle, the maximum amount that can be claimed is the total costs, known as cost capping.

Logbook method, sec. 8 para.. 2 sentence 4 EStG and R 8.1 para. 9 No. 2 LStR:

Here, the value in use is determined using a logbook.

It is important to distinguish between business and professional use.

VAT treatment

For VAT treatment, the transfer of a motor vehicle to an employee is a supply for consideration in the form of a transaction similar to an exchange within the meaning of sec. 3 para. 12 sentence 2 UStG, cf. sec. 15.23 para. 8 to 11 UStAE (see VAT Newsletter 37/2022: German Federal Fiscal Court: No turnaround in the taxation of company cars). The taxable amount is based on the value of the other transaction, sec. 10 para. 2 sentence 2 UStG. In the case of the transfer of a motor vehicle, this is the total expenditure for the transfer. This can be determined by means of an estimate, sec. 15.23 para. 10 UStAE. For reasons of simplification, however, the determined income tax values may also be used, provided that the vehicle is not an electric or hybrid vehicle; sec. 1.8 para. 8 in connection with 15.23 para. 11 UStAE in connection with R 8.1 para. 9 LStR.

If a company car is used by a sole trader, the minimum use requirement under sec. 15 para. 1 sentence 2 UStG must be observed when exercising the allocation option.

See VAT Newsletter 04/2023: German Federal Fiscal Court restricts input VAT deduction for luxury cars

Hybrid, electric vehicles and electric bicycles

In a letter dated 7 February 2022, the Federal Ministry of Finance extended sec. 15.23, para. 1, sentence 1 UStAE to hybrid and electric vehicles with a maximum speed of 50 km/h and electric bicycles if they are subject to registration, insurance or driving licence requirements. In addition, a corresponding application of sec. 15.23 UStAE for (electric) vehicles not subject to registration, insurance or driving licence requirements was added by a new sec. 15.24 UStAE.

It is important to note that the income tax benefits for electric and hybrid cars (the so-called 0.25% and 0.5% regulations) do not apply for VAT treatment!

See VAT Newsletter 06/2022: German Federal Ministry of Finance on the private use of electric/hybrid vehicles and bicycles

Change in the assessment method

In the Federal Ministry of Finance’s letter dated 3 March 2022, a retroactive change in the wage tax deduction for the entire calendar year prior to the submission of the wage tax statement was permitted, particularly in light of the increased incidence of working from home and business trips.

When changing the assessment method, the VAT treatment should also be taken into account!

Discover our digital solution: Company Car Tax Back

Events

An event can take many different forms. Many different occasions and guests can be considered. The following points, among others, must be taken into account for tax treatment:

For income tax purposes, the possibility of deducting business expenses,

for income tax purposes, a potentially taxable monetary benefit for employees, and

for VAT purposes, the right to deduct input VAT or the tax liability for a supply carried out free of charge.

An overall event may not have any reward character at all, or it may include individual elements of enrichment (meals, gifts) or even be assessed as an incentive/gift in its entirety.

For a correct classification, it is important to be clear about the reason, the programme and the guests. In particular, sufficient documentation should be provided.

Numerous guidelines from the tax authorities (Federal Ministry of Finance’s letters, rulings) have been published on the possible arrangements for events (e.g. VIP boxes, business seats, etc.), and judgments (e.g. Federal Fiscal Court, judgment of 23 November 2023 – VI R 15/21) have been issued, which should be used as a guide.

Company events

Example

The following points must be checked in relation to income tax in accordance with sec. 19 (1) no. 1a EStG:

1. Is it conceptually a company event?

2. Is the EUR 110 allowance exceeded?

For VAT treatment, it depends on whether the benefits provided at the company event are within the usual limits. This is assumed to be the case up to an amount of EUR 110 including VAT. But be careful: for VAT treatment, there is no allowance, but an exemption limit! If the expenses per employee exceed the exemption limit, the deduction of input VAT is excluded in full.

For VAT treatment, events/parties for individual employees are not considered business events!

See VAT Newsletter 22/2015: Umsatzsteuerliche Konsequenzen der lohnsteuerlichen Änderungen für Betriebsveranstaltungen und Aufmerksamkeiten

Contact