Influencers – initially dismissed by some as a passing fad, they are now an integral part of the media landscape. Companies across all industries are leveraging their reach to promote their products. Corporate budgets for influencer marketing have been rising sharply for years and are set to increase further in the future.

VAT assessment

As companies' spending increases, so do influencers' transactions and the importance of assessing the underlying facts for VAT purposes. Incorrect VAT assessment or even failure to report the transactions generated can have serious consequences, as a recent example shows: The tax investigation department of the North Rhine-Westphalia tax authorities has set up a special ‘influencer team’ to focus on tax evasion by influencers.

This being said, the following issues need to be clarified:

Taxable status of influencers

Taxable amount and supplies of goods and services for consideration

Exchange of invoices between companies and influencers

Deduction of input VAT for companies and influencers

Is flat-rate taxation applicable for direct tax purposes?

Taxable person – when is an influencer a taxable person?

The status of a taxable person is determined in accordance with sec. 2 para.1 sentence 1 of the German VAT Act (UStG). A taxable person is anyone who independently performs a business or professional services.

According to sec. 2 para. 1 sentence 3 UStG, the service must be performed on a long-term basis and with the intention of generating income. A service is considered to be continuous if it is designed to generate consideration on a permanent basis, cf. sec. 2.3 para. 5 sentence 1 of the German Administrative VAT Guidelines (UStAE). The following points in particular can be used as indicators for this (German Federal Fiscal Court, judgment of 19 July 1991 – V R 86/87):

the systematic nature of the activity,

the intention to repeat it,

participation in the market,

the intensity of the activity and

the external appearance.

Influencers usually create what is known as content. The creation of content can be seen as a supply to the company they are promoting. The exact point in time at which the influencer's service can be regarded as business activity is difficult to determine and is subject to dispute with the tax authorities.

In addition, especially at the beginning of a career as an influencer, it is important to bear in mind the German VAT Act pursuant to sec. 19, which provides for an exemption for small enterprises.

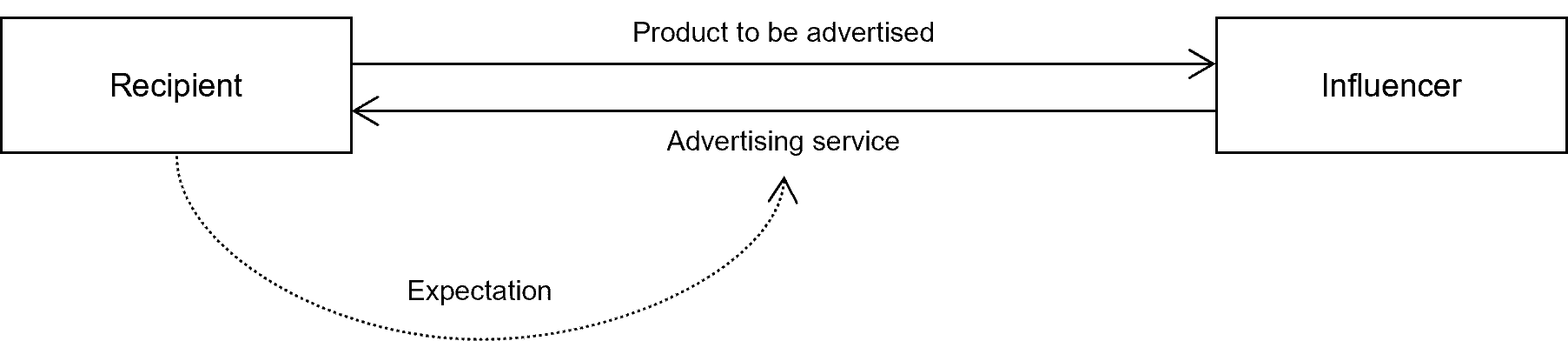

Taxable amount and supplies of goods and services for consideration – which transactions are relevant for VAT purposes?

A supply of goods and services for consideration within the meaning of sec. 1 para. 1 no. 1 UStG, which may lead to VAT liability, requires an act for remuneration. For reasons of determinability of the remunerations, there must be a direct, individually identifiable connection, cf. ECJ judgment of 27 March 2014 – Case C‑151/13 – Le Rayon D‘Or. In addition, the actions of the taxable person must confer an economic advantage on the other person.

Example 1 – remuneration exclusively in money:

The influencer creates an advertising post for the recipient for their product. For creating the advertising post, the influencer receives remuneration in the amount of EUR X plus 19% VAT. The influencer must return the product to the recipient immediately after creating the content.

The advertising service provided by the influencer constitutes a supply of services within the meaning of sec. 3 para. 9 sentence 1 UStG. Accordingly, the fee he receives for providing the advertising service is subject to VAT. The influencer is therefore obliged to pay the 19% VAT to the financial authorities. The provision of the product, on the other hand, is a non-taxable provision. This is irrelevant for VAT purposes.

In the lack of a specific provision in sec. 3a para. 3 to 8 or in secs. 3b and 3e UStG, the place of supply is determined pursuant to sec. 3a para. 2 UStG – the place of supply is therefore at the registered office of the recipient (the advertised company). The recipient is generally entitled to deduct input VAT from the advertising services received in accordance with sec. 15 para. 1 sentence 1 no. 1 UStG. However, this requires a proper invoice, sec. 15 para. 1 sentence 1 no. 1 sentence 2 UStG.

If the recipient is based in another EU Member State, the reverse charge mechanism must be considered.

However, if the recipient is based in a third country, this may have significant consequences for the influencer.

Example 2 – Barter deal: remuneration exclusively in goods:

As in the examples above, the influencer creates an advertising posting for the recipient for their product. Instead of monetary compensation, the influencer receives the advertised product worth EUR X plus 19% VAT. The influencer also uses the advertised product privately.

The present example concerns a barter deal within the meaning of sec. 3 para. 12 sentence 2 UStG. The prerequisite for the assumption of a barter transaction is that two supplies for consideration within the meaning of sec. 1 para. 1 no. 1 UStG are opposed to each other, which are linked only by the modality of the agreement on consideration (Federal Fiscal Court, judgment of 6 December 2017 – V R 42/06). It follows from sec. 10 para. 2 sentence 2 UStG that in the case of a transaction similar to an exchange pursuant to sec. 3 para. 12 UStG, the value of each transaction is deemed to be the consideration for the other transaction. Thus, the value of the influencer's advertising service is measured by the fair market value of the product to be advertised.

According to sec. 15 para. 1 no. 1 UStG, both the influencer and the recipient are entitled to deduct input VAT in this case. The prerequisite is again that the parties involved are in possession of a proper invoice. In the case of influencers, the problem arises that the item is also used privately. Whether, and if so, to what extent the influencer can claim input VAT must be decided on a case-by-case basis. This question is often a point of contention with the tax authorities.

Example 3 – Mixed remuneration consisting of money and goods:

The influencer creates an advertising post for the recipient for their product. For creating the advertising post, they receive remuneration in the amount of EUR X plus 19% VAT with the product to be advertised (value: EUR Y net).

The VAT assessment depends on the terms and conditions of the contract between the influencer and the recipient:

Option 1: Agreement on a permanent loan:

As in the first example, the advertising service provided by the influencer – the advertising post – constitutes a supply of services within the meaning of sec. 3 para. 9 sentence 1 UStG. Accordingly, the fee of EUR X received by the influencer for providing the advertising service is subject to VAT at a rate of 19%, sec. 1 para. 1 no. 1 UStG. The influencer is therefore obliged to pay VAT to the tax authorities. However, it is problematic whether the permanent loan of the product is part of the VAT base or qualifies as a non-taxable provision.

Option 2: The influencer may permanently keep the advertised product:

The remuneration of the influencer in money with the product to be advertised, which the influencer may keep beyond the creation of the content, constitutes a barter transaction including an additional cash payment according to sec. 1 para. 1 no. 1 sentence 1 UStG in connection with sec. 3 para. 12 sentence 2 UStG. In this example, too, the influencer is liable to VAT on a supply without consideration in accordance with sec. 3 para. 9a no. 1 UStG if the previously advertised product is used for private purposes and if input VAT was deducted.

The contractual arrangement is of crucial importance!

Example 4 – Gifts:

The recipient sends the influencer a product worth EUR X net, plus 19% VAT, as a gift. They expect the influencer to promote the product for them in an effective manner.

With regard to the question of how supplies made by an influencer without a specific contract but which constitute remuneration for a product are to be treated for VAT purposes, there is neither supreme court jurisprudence nor specific guidance from the tax authorities. In this case, interpretation on a case-by-case basis is required.

Example 5 – Hotel invitation:

An influencer receives an invitation to stay at a hotel with a total value of EUR X gross. In return, the influencer provides advertising services to the hotel by creating appropriate advertising content.

This again constitutes a barter deal according to sec. 3 para. 12 sentence 2 UStG. The hotel must issue an invoice showing VAT to the influencer as the recipient of the service. The influencer is generally entitled to claim the input VAT from this invoice.

In return, the influencer also provides the hotel with a supply of services in the form of advertising. He is therefore also obliged to issue an invoice to the hotel showing VAT. The influencer's supply is measured according to the value of the trip.

In such cases – especially in cross-border cases – the place of supply must be taken into account.

The influencer may be obliged to register for VAT in the country.

Example 6 – OnlyFans, Twitch, TikTok, YouTube and similar social media platforms

The VAT treatment of income earned on OnlyFans and other social media platforms such as TikTok, YouTube and Twitch was recently the subject of a ruling by the ECJ. On such platforms, content creators offer exclusive content that customers can only view if they subscribe. In the case of Fenix International Ltd. (judgment of 28 February 2023 – C-695/20), it was clarified who provides the service to the end customer: the content creator (service provider) or the platform within the framework of a deemed supply chain of services (purely for VAT purposes). This question served to identify who is liable for VAT on the entertainment service provided to the end customer.

In its judgment, the ECJ confirmed the application of the chain of supply fiction pursuant to Art. 9a sec. 1 of the VAT Directive in connection with Art. 28 of the VAT Directive. In particular, Art. 9a sec. 1 of the VAT Directive is legally valid, as it merely clarifies the VAT Directive without amending or even changing it. This means that the platform or portal operator is part of the supply chain between the content creator and the end customer. This assumption represents the economic and commercial reality: the platform irrefutably acts in its own name and on behalf of others as soon as it authorises invoicing to the recipient of the service, approves the provision of the service or sets out the general terms and conditions for the provision of the service.

From the perspective of German content creators, the judgment is very welcome: they can now argue to OnlyFans and similar platforms that they provide B2B services to the platform pursuant to sec. 3a para. 2 UStG and not supplies to followers. If the platform is based abroad, this means that the transactions are not taxable in Germany. Anyone who has paid VAT in Germany can claim a refund!

Donations

Another example of platform income for influencers is so-called donations, such as those regularly paid on Twitch. There are good reasons to take the view that these donations are also not subject to VAT in Germany according to the principles of the ECJ's OnlyFans ruling (contrary to the Düsseldorf Fiscal Court).

Deduction of input VAT by the parties involved – what rights do influencers have?

Substantive legal requirements for the deduction of input VAT

Under the conditions of sec. 15 para. 1 no. 1 UStG, the parties involved may deduct the VAT legally owed as input VAT insofar as they procure goods and services from a company for their business. According to sec. 15 para. 1 no. 1 sentence 1 UStG, the deduction of input VAT requires, among other things, that the recipient of the supply receives the supply ‘for his business’. This means that the company must intend to use the supplies received for its business activities in order to provide supplies for consideration, see sec. 15.2b para. 2 sentence 1 UStAE. This is the case if there is a direct and immediate connection with taxable transactions, see sec. 15.2b para. 2 sentence 3 UStAE.

The remuneration in goods is directly and immediately related to the creation of content by the influencer and the resulting promotion of the products. The influencer is therefore entitled to deduct input VAT on the supplies received. The recipient of the advertising service provided by the influencer is also entitled to deduct input VAT on the basis of the supply received.

The influencer is often denied the deduction of input VAT on the grounds that the products are used for purely private purposes after being advertised. An online shop run by the influencer can provide a remedy insofar. With clever structuring, input VAT can be claimed for the products. At the same time, the inflow is not subject to income tax, as the products are business expenses/cost of goods sold.

Problems can arise here if transactions have been classified incorrectly or incorrectly for VAT purposes.

Proper invoice

A deduction of input VAT without an invoice is not possible, see Federal Ministry of Finance’s letter dated 18 September 2020. This also follows from sec. 15 para. 1 no. 1 sentence 2 UStG, which states that the exercise of the right to deduct input VAT requires that the company has an invoice issued in accordance with secs. 14, 14a UStG. According to sec. 14 para. 4 UStG, a proper invoice must contain, among other things, the following information:

No. 1: Name and address of the supplier and the recipient of the supply

No. 2: VAT ID number of the supplier

No. 5: Quantity and type (standard commercial designation) of the goods supplied or the scope and type of supply of services

No. 8: VAT rate applicable to the supply.

According to sec. 14 para. 6 no. 3 UStG, regulations may provide for simplifications whereby certain information pursuant to sec. 14 para. 4 UStG does not have to be included in the invoice. The legislator has made use of this authorisation in sec. 33 of the German VAT Implementation Code – invoices for small amounts (> EUR 250) only need to contain certain information specified in sec. 14 para. 4 UStG.

Practice shows that invoices are often not issued in the influencer sector. This means that the parties involved are not entitled to deduct input VAT in the absence of an invoice. However, each party has the option of securing the deduction of input VAT for both parties.

In practice, a missing invoice must be distinguished from an incorrect invoice, which only lacks the mandatory invoice details specified in sec. 14 para. 4 UStG.

The changes in the context of the digitisation of VAT must be observed.

Current developments

Influencers – will we soon see advertising for bars, or rather advertising behind prison bars?

The tax authorities in North Rhine-Westphalia are taking a close look at influencers. A special tax investigation unit has been set up – the Influencer Team – to uncover tax losses estimated at €300 million only in North Rhine-Westphalia. The VAT treatment of influencers and their supplies is currently coming under increased scrutiny.

Contact