Where goods are bought and sold in large volumes, central clearing agents often act as intermediaries between suppliers and companies affiliated with the central clearing agent. These affiliated companies hope that by bundling demand, they will obtain better terms when purchasing goods from suppliers. The central clearing business is based on numerous different payment and supply relationships. The central clearing agent usually provides the following services:

Central settlement

Assumption of the liability

Sales promotion, bundling of purchasing volumes, market access, centralisation of price negotiations, in practice usually remunerated by additional payments from suppliers. These are referred to in various ways (group bonus, special bonus, ‘additional bonuses’, additional account, etc.)

The central settlement business has the special feature that the central settlement agencies pass on the consideration for their supplies – central settlement, credit protection and sales promotion – to their member companies/affiliated companies. The central settlement agency is usually financed by membership fees/consideration paid separately by the member companies/affiliated companies.

Centralised settlement in the focus of jurisprudence and tax authorities

Although centralised settlement is widespread in business practice, it has long been neglected in VAT law. However, this changed abruptly with the so-called Ibero Tours decision of the European Court of Justice (judgment of 16 January 2014, Case C-300/12, Ibero Tours) and the judgment of the German Federal Fiscal Court (judgment of 3 July 2014, V R 3/12). The changed legal opinion from the aforementioned judgments was adopted by the tax authorities (Federal Ministry of Finance’s letter of 27 February 2015). Even more than a decade after these judgments, central settlement remains a key issue in VAT jurisprudence, not least due to the recent judgments of the Federal Fiscal Court (judgment of 23 October 2024, XI R 6/22; judgment of 29 August 2024, V R 20/23). These confirm the changed view.

The judgments from 2014 and the Federal Ministry of Finance’s letter on the matter led to a new legal situation with regard to the VAT treatment of supply relationships. As a result, significant adjustments were necessary for all parties involved – goods suppliers, central settlement providers and affiliated companies. Anyone who does not comply with this legal opinion risks horrendous additional payments and VAT consequences.

Basics of central settlement

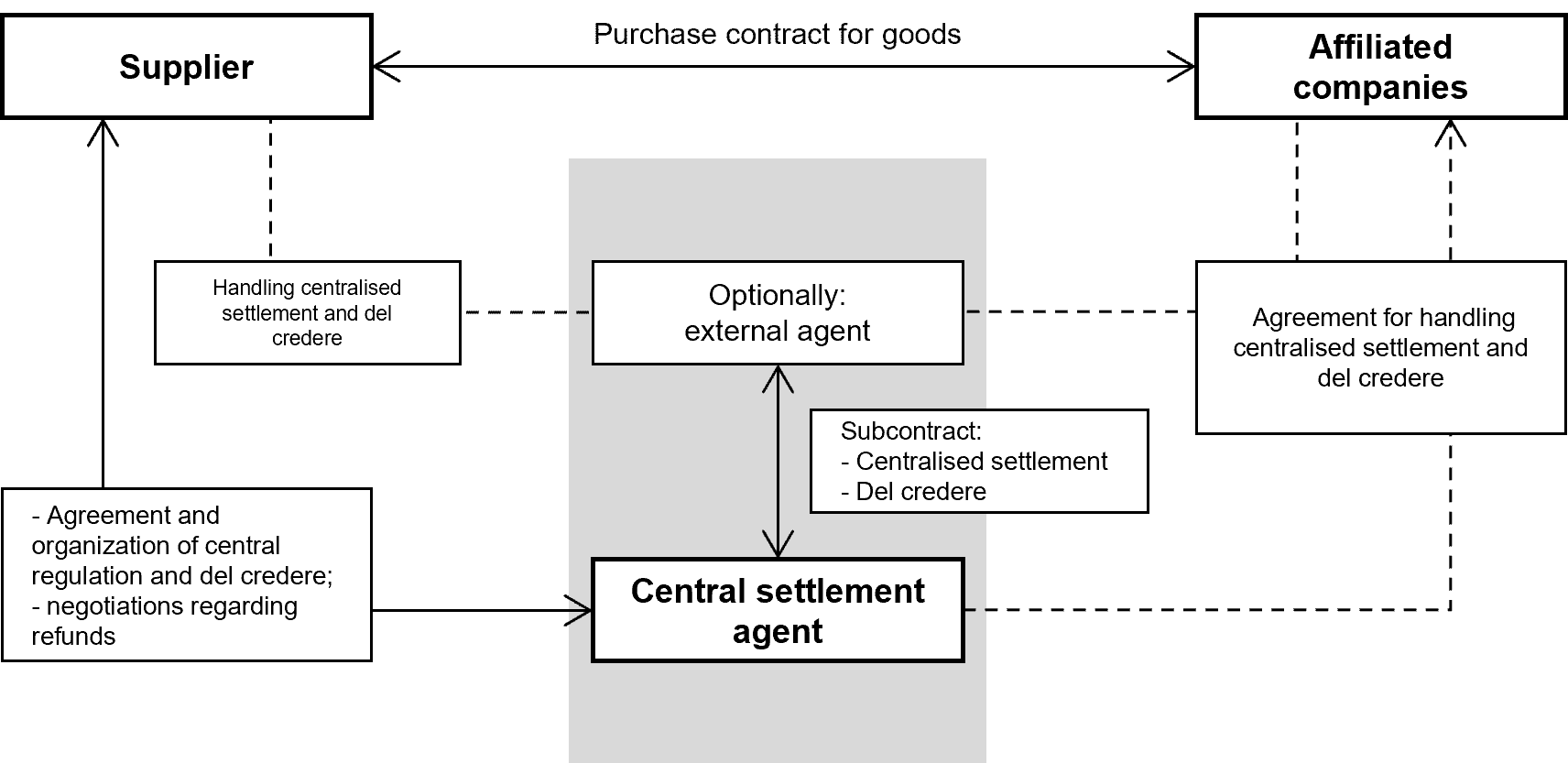

Central settlement is a process in which a central entity, the central settlement agent, handles all invoice processing between member companies/affiliated companies and their suppliers. The central settlement agent collects the invoices and settles them in batches with the suppliers on time, usually after deducting agreed discounts. The central settlement agent then collects the amounts from the affiliated companies.

In addition to simply forwarding payments (central settlement), the central settlement agent often also assumes the del credere. Del credere is a contractually agreed liability that secures the solvency of a third party. In this case, the central settlement agent is obliged to the supplier for any payment defaults by the affiliated company if the latter fails to meet its obligations. The del credere liability can be applied to a specific transaction (specific del credere) or a specific customer (general del credere).

In practice, there is a variety of del credere solutions. In addition to the classic payment guarantee, joint and several liability can be agreed alongside the debtor (affiliated company). In addition, it is also possible for the central settlement agent to acquire its member's liability during the payment process by purchasing the claim. In practice, the central settlement agent does not always ultimately assume the del credere risk itself. The del credere can be assumed by a bank, for example, on behalf of the central settlement agent.

The process can be simplified and illustrated as follows:

Bonuses for central settlement

Central settlement agents and purchasing associations often receive additional payments from suppliers in addition to the fees for central settlement, with or without del credere. In practice, these payments are referred to in very different ways, e.g. as group bonuses, special bonuses or additional accounts. What these constellations have in common is that the central settlement agent passes on these amounts in full to the member companies/affiliated companies. In this respect, there is no difference between these payments and the supplies in the form of central settlement and del credere. With these group bonuses, the suppliers compensate the central settlement agent for economic advantages such as sales promotion, bundling of purchase volumes, granting market access and centralisation of price negotiations. The central settlement agent collects these amounts in its own name and on its own account.

These special bonuses are not to be confused with the bonuses to which the member company/affiliated company of the central settlement agent is directly entitled (so-called house bonuses). Payment transactions for these ‘normal’ bonuses are also handled by the central settlement agent. In contrast to group bonuses, ordinary bonuses are related to the purchase of goods by the affiliated companies and do not constitute a separate supply.

VAT treatment

The supply and service amounts are based on the following service exchange relationships:

Supplier and affiliated company/member company:

Delivery of goods by the supplier: Supply subject to VAT

Granting of discounts/house bonuses: VAT-deductible discounts or reductions in consideration pursuant to sec. 17 of the German VAT Act (UStG)

Affiliated company/member company and central settlement agent:

Central settlement: The central settlement agent regularly provides its affiliated companies/member companies with supplies of services in the form of central settlement. The capital resources of the central settlement agent are handled differently in practice. The central settlement agent is often financed by separate consideration paid by the affiliated companies/member companies. This enables the central settlement agent to pass on the other benefits to its affiliated companies/member companies in full.

Other agreements: In exceptional cases, there are further agreements between the central settlement agent and the affiliated company/member company which may give rise to a relationship of exchange of services. In practice, for example, special advertising obligations for certain products in return for consideration can be observed, which result in a taxable supply of services by the affiliated company.

Central settlement agent and supplier:

Central settlement: Central settlement constitutes a supply of services by the central settlement agent to the supplier.

Del credere: The take over of the del credere constitutes a supply of services by the central settlement agent to the supplier. This is generally a VAT exempt financial service. However, it is subject to an option pursuant to sec. 9 UStG. In practice, the supply is generally invoiced as taxable, as the parties involved are entitled to deduct input VAT without restriction.

Group bonus: The advantages accruing to the supplier from the services of the central settlement agent give rise to a supply of services if a so-called group bonus is paid to the central settlement agent.

The VAT issues arise mainly from the assessment of the passing on of the benefits by the central settlement agent to its affiliated companies/member companies. See the separate section on this below.

Transfer of benefits by the central settlement agent

Usually, the central settlement agent passes on the benefits to which it is entitled in its own name and on its own account to its affiliated companies/member companies. This applies to consideration for central settlement, del credere and group bonuses.

In the first step, there is no doubt that the central settlement agent provided supplies of services to the suppliers. For decades, central settlement agents treated the forwarding of the amounts as a reduction of the taxable amount pursuant to sec. 17 UStG (= reduced their own VAT liability). The affiliated companies had correspondingly reduced the deduction of input VAT from the purchase of goods from the suppliers, even though the purchase of goods by the affiliated company from the suppliers was a completely different service relationship (= VAT paid back to the tax authorities). For the tax authorities, this treatment was a zero-sum game.

The changed jurisprudence now applies precisely to the point at which the central settlement agent passes on the benefits. In its judgment of 16 January 2024, the ECJ denied the existence of a reduction in remuneration if a travel agency passes on part of its commission to the traveller (Case C-300/12 – Ibero Tours). The discount granted by the travel agency to the traveller does not lead to a reduction in remuneration either in the service relationship between the tour operator and the traveller or in the service relationship between the travel agent and the tour operator.

In its judgment of 3 July 2014 (V R 3/12, BStBl. II 2014, 307), the German Federal Fiscal Court ruled that the principles of the ECJ judgment in Ibero Tours also apply to the sector of central settlement. Accordingly, discounts granted by a central settlement agent to its members for the purchase of goods from suppliers do not constitute a reduction in the consideration for the supplies provided by the central settlement agent to the suppliers. Furthermore, the Federal Fiscal Court expressly clarified that the member is not obliged to reduce the deduction of input VAT on the purchase of goods due to the passing on of benefits by the central settlement agent.

The tax authorities commented on the changed jurisprudence of the ECJ and the Federal Fiscal Court in the Federal Ministry of Finance’s letter dated 27 February 2015 – IV D 2 – S 7200/07/10003, BStBl. I 2015, 232. The Federal Ministry of Finance has adopted the view of the changed jurisprudence. As a result, numerous central settlement agents and member companies have changed their settlement procedures. Since then, benefits passed on by the central settlement agent have only been paid to the respective member company net of VAT. Neither the central settlement agent reduced its VAT, nor did the member company reduce its input VAT on the purchase of goods from the supplier.

Current jurisprudence of the German Federal Fiscal Court – back to the beginning?

At that time, from 2014/2015 onwards, as a result of the change in jurisprudence, many affiliated companies/member companies submitted refund applications to the tax authorities and requested that the reduction in input VAT amounts be reversed. Not all of these cases have yet been legally settled.

In 2020, the Fiscal Court of Münster dismissed an appeal by an affiliated company for reversal of the input VAT adjustment. In a departure from the jurisprudence of the ECJ and the Federal Fiscal Court, an economic assessment must be made, deviating from the civil law agreements. According to this, the group bonuses (which are disputed in these proceedings) are economically directly related to the deliveries of goods to the affiliated companies. In essence, these are reductions in the purchase price and not consideration for supplies by the central regulator.

However, the appeal lodged by the affiliated company against the judgment of the Fiscal Court in Münster was successful. The Federal Fiscal Court clearly and stringently presented the development of case law and emphasised that, for VAT purposes, it is crucial whether a discount is granted within or outside a chain of services. In the present case, there was no chain of services. This is because the contractual supplier delivered directly to the affiliated company of the central settlement agent. The central settlement agent, on the other hand, provided a separately assessable supply of services to the contractual supplier. According to the ECJ's Ibero-Tours judgement, this precluded a reduction in remuneration.

Fortunately, the Federal Fiscal Court also addressed the argument put forward by the Münster Fiscal Court. It is correct that the group bonuses passed on are related to the purchase of goods. However, this does not distinguish the case from jurisprudence, but is common practice when intermediaries pass on discounts. After all, the passing on of discounts always has something to do with the transactions brokered. The more recent ECJ judgments on legally prescribed discounts in the pharmaceutical sector do not preclude this conclusion, as there was no legal obligation to grant the discounts in the present case. Similarly, the differences to the Federal Fiscal Court proceedings (Ref.: V R 20/23), in which a central settlement agent appealed, were not relevant to the decision. In these proceedings, the Federal Fiscal Court also ruled that passed-on group bonuses are not subject to VAT and that the central settlement agent cannot reduce its VAT on supplies to the suppliers..

Consequences for practical application – urgent action and clarity at the same time

Not all affected parties have implemented the far-reaching changes resulting from the change in jurisprudence since 2014. Based on the recent ruling by the Federal Fiscal Court, it can now be assumed that the highest court has established case law. The consequences and recommended actions therefore vary for affiliated companies/member companies, central settlement agents and suppliers:

Affiliated companies: They can rejoice in the established jurisprudence. It is now clear that they do not have to reduce the deduction of input VAT on purchases of goods due to payments passed on, which are initially due to the central settlement agent. Following the change in jurisprudence in 2014, numerous refund applications were filed. Many of these proceedings are still pending. With the Federal Fiscal Court's decision, the balance is clearly tipping in favour of the affiliated companies' refund claims.

Central settlement agents: Some central settlement agents have not implemented the change in case law, for example because they believed – as did the Münster Fiscal Court – that they were in a different situation. This decision makes the air thinner and the risk significantly higher. This is because these central settlement agents are still reducing their VAT, possibly unjustifiably. They must review the VAT treatment of their service relationships as quickly as possible and, if necessary, adjust their invoices. This applies both to affiliated companies and to contract suppliers.

Suppliers: The jurisprudence also clarifies that central settlement, del credere and group discounts constitute consideration for the supply of services by the central settlement agent to the suppliers. Suppliers therefore require a proper invoice from the central settlement agent in order to be able to exercise their right to deduct input VAT. In practice, suppliers sometimes treat the benefits they grant to central settlement agents as reductions in the consideration for the goods supplied to the affiliated companies/member companies. This is incorrect and entails considerable risks, as in such cases VAT is reduced on payments without a proper invoice being issued.

Contact