In the recent past, the economic significance of cryptocurrencies has experienced a considerable upswing. Increasing social and political acceptance, such as the recent approval of the first Bitcoin ETF by the US Securities and Exchange Commission, with steady technological progress are leading to the continuous growth of new blockchain-based business models.

However, these new technologies also bring challenges, particularly in the sector of tax law. Our existing tax laws, which arose in a pre-internet era, are now confronted with a completely new, decentralised financial system. This system consists of anonymous users whose assets are represented by fungible and non-fungible tokens (NFTs), and transactions that are no longer verified by traditional banks but by global mining and staking pools.

In the dynamic world of cryptocurrencies, NFTs and the metaverse, new VAT issues are constantly arising. The following aspects are particularly important for token-based blockchain business models:

1. Determining the place of supply for unknown recipients

2. Transaction validation through mining and staking pools

3. Trading in fungible and non-fungible tokens (NFTs)

4. The right to deduction of input VAT

5. Service relationships in liquidity pools in the DeFi (Decentralized Finance) sector

6. Airdrops

Several questions regarding income tax were clarified in the Federal Ministry of Finance’s letter dated 10 May 2022. The Federal Ministry of Finance’s letter dated 27 February 2018 regarding VAT was issued following the ECJ ruling in the Hedqvist case (KMLZ VAT Newsletter 11│2018). It is essentially limited to the validation of transactions through computing power (mining) and the exchange of conventional currencies (fiat money) into cryptocurrencies and vice versa. Consequently, the tax authorities have not yet addressed the sectors of non-fungible tokens (NFTs), validation of transactions through so-called staking pools, ‘donations’ of tokens (airdrops), metaverse transactions and many others in terms of VAT. However, according to reports, the tax authorities are gearing up internally and forming expert groups for the sales taxation of the crypto world.

Where is the place of supply for unknown recipients of services?

In the traditional financial world, the place of supply is usually determined simply on the basis of the geographical location and physical presence of the parties involved. This poses a much more complex challenge in the world of cryptocurrencies and blockchain. Users of blockchain networks such as Ethereum or other EVM-based networks are often spread across the globe and operate solely under the pseudonym of their crypto wallet addresses. For example, the crypto wallet address is ‘0x287929348C2f20Eec3473...’ and does not allow any conclusions to be drawn about the location of the party involved.

What is a wallet address?

The wallet address works much like a transparent locker – the contents are visible to everyone, but only the owner with the correct key can access them and carry out transactions. Your own tokens are not stored in the wallet. The tokens are located on the respective blockchain. The wallet merely allows you to access the tokens.

What is the problem regarding to VAT?

In the case of a service provided electronically, such as the transfer of tokens or the validation of transactions, the place of supply is determined by the location of the recipient of the service. This applies to both private (§ 3a para. 5 sentence 1 German VAT Act) and business (§ 3a para. 2 German VAT Act) recipients of services.

If the pseudonymisation of the wallet address cannot be broken down due to a lack of further information, there is a risk that the general principles of case law (e.g. the Federal Fiscal Court decision of 28 November 2017) will be applied to determine the recipient's location. In the opinion of the BFH, the inability to provide proof of a foreign recipient location results in domestic residency. In other words, if it cannot be proven that the customer is located abroad, they are considered to be resident in the same country. The consequence is that German VAT arises. In many cases, the business model is no longer economically viable under these conditions.

In contrast to the Federal Fiscal Court, the Cologne Fiscal Court (judgment of 13 August 2019 – 8 K 1565/18) saw the possibility of estimation pursuant to sec 162 para. 1 sentence 1 of the German Fiscal Code (AO) in the case of the leasing of virtual land. Using conclusive, economically feasible and plausible assumptions, it was possible to estimate the number of customers resident in Germany.

In light of this decision, every indication regarding the customer's place of residence should be used. This is because a blanket assumption that all recipients of services from blockchain-based business models are based in Germany is neither conclusive nor plausible.

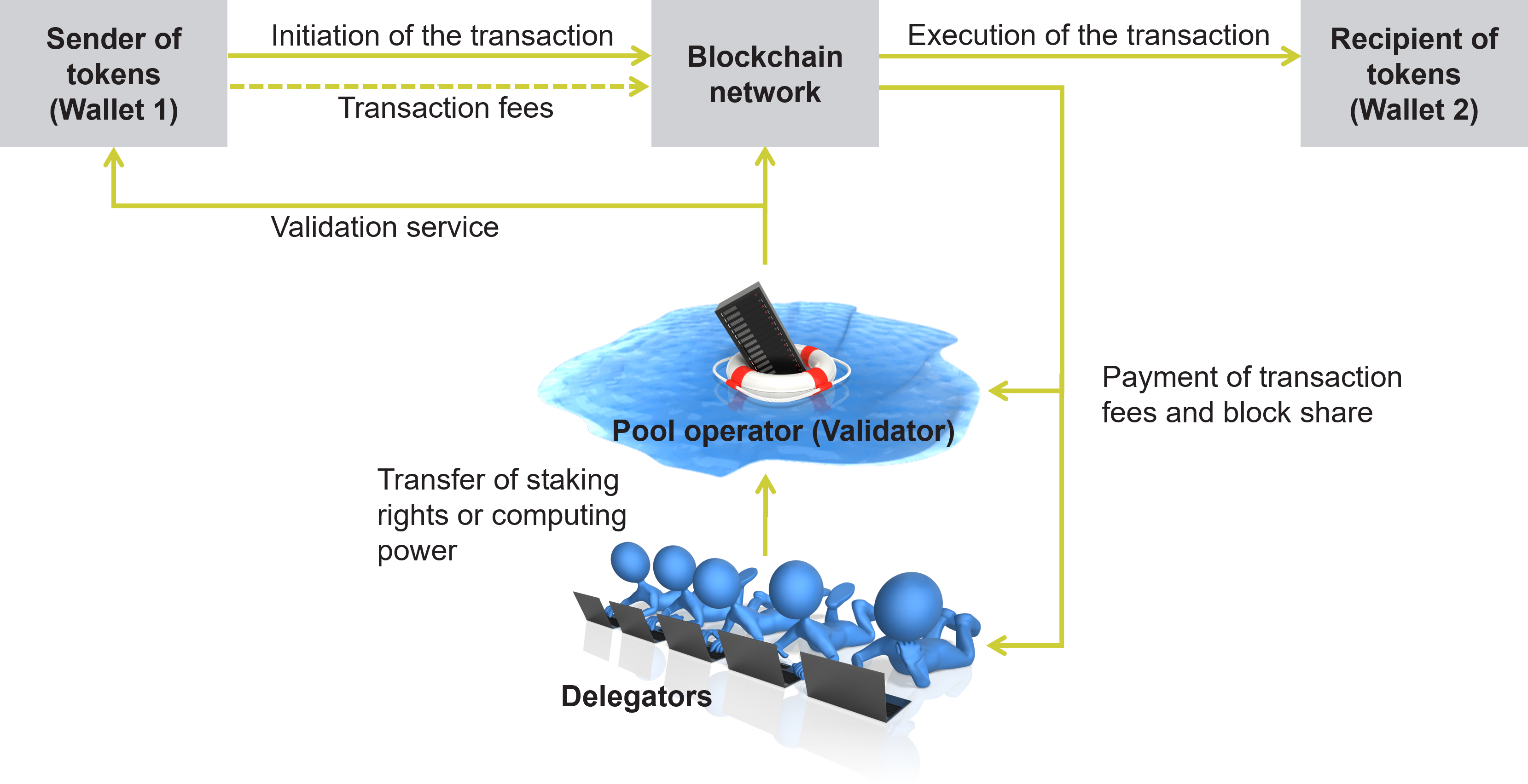

Transaction validation through mining and staking pools?

The proactive participation of blockchain companies in their own mining and staking pools is of strategic importance. This involvement not only enables a stronger market position, but also contributes crucially to the security and decentralisation of blockchain technology. In practice, this raises numerous questions, particularly with regard to service relationships and the right to a deduction of input VAT.

How does transaction validation work?

In blockchain, the best-known form of distributed ledger technology, transactions are verified by validators. These validators operate nodes that serve as hubs in the blockchain network. Since individuals often do not have the necessary computing power or number of tokens for effective solo mining or staking, pools are formed. Here, users pool their resources, thereby increasing their chances of adding blocks to the blockchain and validating transactions. When a transaction is validated, rewards are paid for it.

What are the performance relationships between the network, the validators and the delegators?

When validating transactions in mining and staking pools, where delegators transfer their computing power or staking rights, the question arises as to whether this supply is provided by the pool operator or the delegators to the blockchain network and the transaction senders. Determining the service relationships is complex and depends on the specific design of a network.

1. The economic reality regularly points to a supply provided by the pool operator to the blockchain network or to the transaction senders. Only the pool operator is in a position to provide the validation supply in the first place. This is because only the pool operator provides the technical infrastructure for validating transactions and updating the blockchain by operating a node.

2. The computing power transferred by a delegator or the staking rights merely increase the probability that the pool operator will be selected by the blockchain network as a block creator, so that the validation service can only be provided by the pool as a whole in terms of computing power or staking rights.

3. In addition to the economic reality, the so-called shop law can also argue in favour of the provision of services by the pool operator.

Why is it necessary to differentiate between the supply provided to the network and the transaction sender?

To the network in exchange for block share: Non-taxable transactions (recipient not identifiable).

To the sender in exchange for transaction fees: Taxable transactions.

The block rewards, consisting of the block share and transaction fees, constitute the remuneration for the validation service. While the pool operator stabilises and decentralises the entire blockchain network by operating its node and storing transactions, this benefits not only individual transaction senders, but the network as a whole.

Since the network has no individual, identifiable features such as a wallet address, the validation service cannot be controlled vis-à-vis the network, in contrast to individual transaction senders, who are basically identifiable by their wallet addresses.

Is the validator entitled to deduct input VAT?

Due to the non-taxable transactions regarding the block share and the taxable person regarding the transaction fees, the validator is faced with the question of whether and to what extent it is entitled to deduct input VAT.

The crucial factor for the right to the deduction of input VAT is whether there is a direct and immediate connection between the non-taxable validation service provided to the blockchain network regarding the block share and the taxable transactions of the validation service provided to the transaction senders with regard to the transaction fees.

It is practically impossible to provide a validation service only against the block share and without receiving the transaction fees already paid for the validation of transaction senders. In most cases, the costs of the validation service to the blockchain network in relation to the block share are inseparably linked to those of the validation service to the transaction senders. As a result, the full amount of the total expenses is eligible for deduction of input VAT.

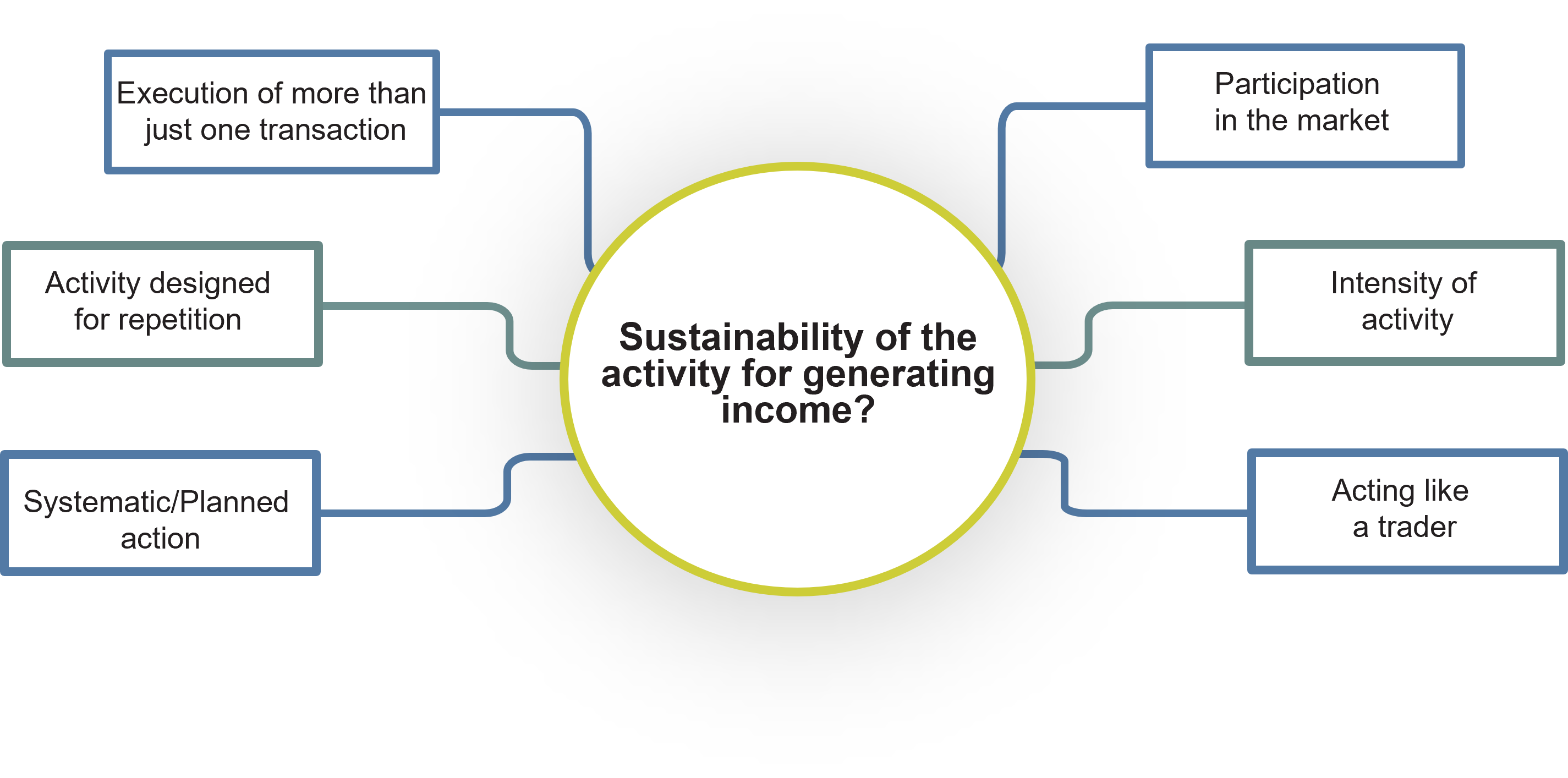

Taxable Person Status in the Context of Delegated Staking Rights?

The transfer of the delegator's staking rights to the validating pool operator constitutes a supply of service pursuant to sec. 3 para. 9 of the German VAT Act (UStG). In return, the delegator receives remuneration which, depending on the arrangement, is paid either directly by the pool operator or by a third party via the blockchain network.

In providing its service to the pool operator, the delegator uses the staking rights arising from its holdings, so there is good reasoning not to qualify the service as going beyond the collection of benefits from its own assets.

If the delegator did not engage in staking, some cryptocurrencies would be at risk of dilution through annual inflation specified in the programme code, due to the addition of new tokens as an incentive for transaction validation. In this respect, the delegator's income could be similar to that of a saver, as maintaining current, building society and savings accounts does not constitute a taxable activity.

On the other hand, the delegation of computing power that goes beyond private use may, depending on the overall circumstances, constitute a sustainable service for generating income.

In what ways does trading differ for currency, utility tokens and NFTs?

Trading in different types of tokens – currency tokens, utility tokens and NFTs – varies significantly. Currency tokens, such as Bitcoin or Ether, primarily serve as digital means of payment. In contrast, utility tokens offer rights of use or the possibility of exchanging them for goods or supplies of services. NFTs (non-fungible tokens) represent a category of their own; they represent unique, non-exchangeable assets. NFTs have recently become very well known in the art world, but they extend beyond this sector and can also function as utility tokens. This is the case, for example, when they represent a share in a company and are linked to specific rights such as dividend entitlements. These diverse applications make the VAT assessment of NFTs particularly complex and dependent on the individual case.

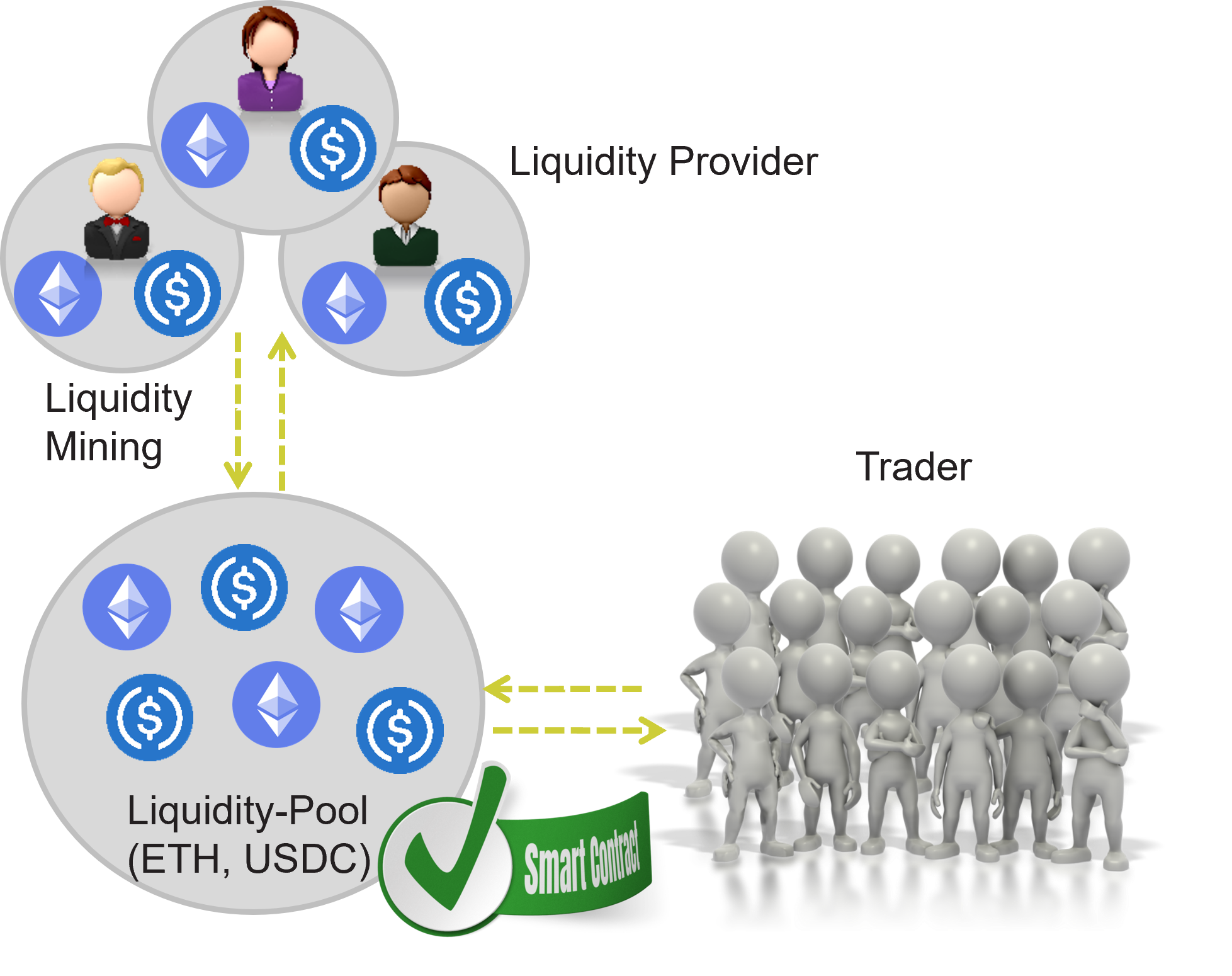

Liquidity mining in decentralized finance?

Liquidity mining in the world of decentralised finance (DeFi) is a key concept for blockchain companies that offer their own tokens on decentralised exchanges. By providing liquidity on these platforms, users can invest in the tokens and participate in the growth of the company.

Example: A new token-based company enters the market. Many users are enthusiastic about the white paper and want to invest in the company tokens. Typically, the company will sell the tokens to interested parties via a token launchpad and, after the sale, install a liquidity pool on various decentralised exchanges so that the tokens can be bought and sold.

Process:

At least two different tokens are sent to a liquidity pool (smart contract) of a decentralized exchange (to enable others to swap).

Receipt of proof of liquidity provision in the form of an LP token (v2: fungible, v3: non-fungible) → Liquidity is now active and generates trading fees.

(LP token can additionally be sent to so-called farms to earn additional rewards).

Termination of liquidity provision by returning the LP token and receiving back the two provided token amounts (not the identical tokens, only equivalent in value).

DeFi is revolutionising the traditional financial sector by enabling users to access comprehensive financial services with a simple wallet setup.

The VAT assessment of liquidity mining requires a detailed examination of the service relationships.

A particular challenge here is that the liquidity pool represented by smart contracts does not constitute an identifiable recipient of services. This applies both to the provision of liquidity in exchange for liquidity tokens and to their return.

When traders trade with the liquidity pool and pay fees for doing so, this service is enabled by the entire liquidity of the pool and not by individual providers.

The liquidity pool is crucial because it enables traders to execute transactions with minimal price impact and slippage, provided there is sufficient liquidity. ‘Price impact’ refers to the effect of a trading transaction on the market price, while ‘slippage’ describes the difference between the expected and actual execution price of an order (caused by swaps by other users).

Airdrops

Airdrops are a popular marketing strategy in which tokens are usually distributed free of charge to increase demand and motivate users to exchange the token via a liquidity pool. The issuer aims to increase awareness and potentially increase the value of its tokens. A key aspect of airdrops is the question of whether they are linked to remuneration. The following airdrop categories can be distinguished:

| Standard Airdrop | Airgrab | Reward Airdrop |

| No specific action required | Pure acceptance of an airdrop | Usually involves performing marketing-related tasks (providing personal data, inviting users, rating, etc.) |

|

|

|

Contact