The Federal Fiscal Court (BFH), in its judgment of 14 May 2025, Case No. XI R 23/22, clarified: A taxable person is not personally liable for VAT debts determined by the insolvency administrator. Such liability is to the insolvency estate (so-called defense of limited post-liability). The BFH overturned the previous contrary decision of the Düsseldorf Fiscal Court (see detailed discussion in VAT Newsletter 25 | 2023).

1 Liability in the Context of Insolvency Law

When a business experiences financial distress, VAT obligations remain in force. Unlike certain relief available under income tax law, a taxable person’s VAT obligations generally continue to apply during corporate insolvency. If an insolvent business fails to settle its VAT debts, the tax authorities may seek payment from a liable party – such as the taxable person, managing director, or insolvency administrator. The situation becomes particularly problematic when liability is not limited to the insolvency estate but extends to the private assets of the liable party. Liability for VAT debts may arise from insolvency law and/or tax law provisions. The primary prerequisite for such liability is a breach of duty by the liable party in connection with the VAT debt. The risk of liability is heightened in the VAT-insolvency context because the liable party may be required to simultaneously comply with conflicting obligations under insolvency and tax law. Under tax law, “liability” always means assuming responsibility for another party’s tax debt. In this regard, the BFH had to decide whether a taxable person should be held liable for the VAT debts of an insolvent business that arose solely as a result of action taken by the insolvency administrator.

2 Decision of the Court

The BFH ultimately concluded that a taxable person is not liable for VAT debts arising in this manner during the course of ongoing insolvency proceedings. Such externally determined liability, in the absence of any personal contribution, is considered legally questionable by the BFH – both in light of the constitutionally protected right to economic self-determination (Art. 2(1) in conjunction with Art. 1(1) of the German Constitution) and in the context of the statutory objective of enabling a fresh economic start according to sec. 1 sentence 2 of the Insolvency Code (InsO).

Accordingly, post-liability for VAT debts is limited to the insolvency estate and fundamentally differs from liability for income tax debts. While the latter is based on pre-insolvency value developments – such as the realization of hidden reserves during the liquidation of business assets – VAT arises from individual transactions during the insolvency proceedings. These differences, in the BFH’s view, justify a differentiated approach to post-liability under income tax and VAT law.

3 Points of Practical Relevance

It should be noted that a taxable person remains personally liable with private assets for VAT debts arising from insolvency proceedings if these were caused by the taxable person’s own actions. By contrast, VAT debts attributable solely to the insolvency administrator are covered exclusively by the insolvency estate. Following the BFH’s decision in favor of taxable persons, pending appeals in similar cases can now be successfully resolved on their merits.

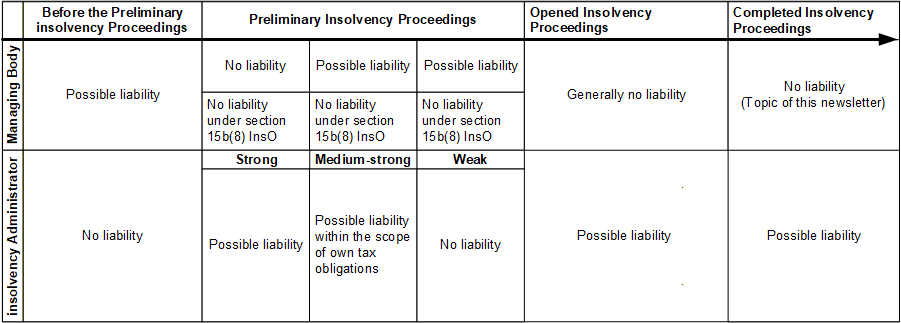

The following table provides a simplified overview of the current status quo of the VAT liability regime under sec. 69 sentence 1, sec. 34, sec. 35 of the German General Fiscal Code (AO) in practice:

The liability of the management body and that of the insolvency administrator are generally mutually exclusive. Under certain conditions, however, the tax authorities may hold an insolvency administrator personally liable for a company’s VAT debts. This requires liability under tax law pursuant to sec. 34 and 69 AO and/or civil law under sec. 60 and 61 InsO, if the administrator, as custodian of the debtor’s assets, culpably breaches VAT payment obligations. While an insolvency administrator is not liable for VAT debts arising after the conclusion of insolvency proceedings, post-liability may apply in individual cases if the relevant VAT debts originated during (preliminary) insolvency proceedings. Of course, in case of absent fault there is no liability here either.