When supplying energy such as electricity, gas, heat, or cooling, there are a few special considerations to bear in mind from a VAT perspective. This is because the German VAT Act contains several provisions that apply specifically to energy supplies. The following questions therefore arise in particular:

Is there an energy supply?

Where is the place of supply of energy?

Is a VAT exemption applicable?

Which does VAT rate apply?

When does the VAT becomes chargeable?

Who is liable for the VAT?

What specific obligations have grid operators and plant operators to consider?

Operation of Battery Storage Systems

1 What is an energy supply and what special cases exist?

A supply within the meaning of the German VAT Act occurs when a taxable person transfers the right to dispose of an item to another person (sec. 3 of the German VAT Act). In addition, not only tangible properties but also intangible assets may form part of a supply, provided they are treated as goods in economic transactions. According to Art. 15 para. 1 of the VAT Directive (MwStSystRL), this applies to electricity, gas, heat, cooling, and similar items. According to the national administrative view, hydropower is also considered as such good (sec. 3.1., para. 1, sentence 2 of the German Administrative VAT Guidelines).

1.1 Special cases

Particular attention must be paid to situations in which the supply of energy is closely linked to another service and has a direct economic connection with it. In such cases, it is necessary to differentiate between the respective energy supply and the circumstances of the individual case (see sec. 4.12.1., para. 5 of the German Administrative VAT Guidelines).

Rental and leasing of immovable property

For example, the supply of heat, electricity, or water may, under certain circumstances, constitute an ancillary service in connection with the rental or leasing of immovable property. In such cases, unlike an independent energy supply, the ancillary service shares the VAT treatment of the main service. In contrast, supplies of heating gas or oil are not considered ancillary services.

However, the German Federal Fiscal Court (BFH) decided in its judgment of July 17, 2024 – XI R 8/21 that the supply of electricity by the landlord to his tenants constitutes an independent service, which is subject to VAT, provided that the tenant is free to choose the electricity supplier and billing is based on consumption. Following the BFH, the Fiscal Court Münster also considered the supply to be independent in its judgment of 18 February 2025 – 15 K 128/21 U. Both courts justify this classification by the legal and factual separation of the electricity supply from the rental agreement. Separate contracts exist, tenants are free to choose their electricity supplier, and the supply serves an independent economic purpose – irrespective of the rental agreement. These decisions therefore deviate from the administrative practice.

Rental of camping spaces

The supply of electricity, heat, or water in connection with the rental of camping spaces is similarly classified (sec. 4.12.3., para. 3, sentence 7 of the German Administrative VAT Guidelines). The assessment depends on the circumstances of each individual case.

Homeowners’ associations and trade fairs/exhibitions/congresses

Special VAT considerations also apply in cases where a homeowners’ association passes on the costs of heat (heating), water, or electricity to its members (sec. 4.13.1., para. 2, sentences 2-6 German Administrative VAT Guidelines). The same applies when an exhibitor at a trade fair, an exhibition, or a congress is not only provided with the exhibition space but also with technical utilities. In other words, when they are supplied with energy such as electricity, gas, or water (sec. 3a.4., para. 2, sentence 2, no. 1 German Administrative VAT Guidelines).

Distance sales

The supply of gas, heat/cooling, and electricity does not constitute a supply the transport is ascribed to. Therefore, according to the current administrative view, such supplies do not qualify as distance sales within the meaning of sec. 3 para. 3a sentence 2 of the German VAT Act, and the related fiction of supply chains does not apply (sec. 3.18., para. 4, sentence 3 of the German Administrative VAT Guidelines). Nor do these energy supplies fall under the definition of intra-Community distance sales as per sec. 3c para. 1 sentence 2 VAT Act (sec. 3c.1., para. 2, sentence 2 of the German Administrative VAT Guidelines).

However, from January 1, 2027, to July 1, 2028, the supply of gas (through a gas network) as well as the supply of electricity, heat, or cooling (via a heating or cooling network) will be treated as intra-Community distance sales. The reform “VAT in the Digital Age” extends the One-Stop-Shop (OSS) from January 1, 2027 (limited until June 30, 2028) to cover such supplies – regardless of the status of the recipient as a taxable person – when carried out by a taxable person not established in the Member State of supply (Art. 2 para. 12 of Council Directive (EU) 2025/516 of March 11, 2025, which introduces a new Art. 369aa into the VAT Directive).

Intra-Community transfer and intra-Community acquisition

Due to the absence of a supply of goods with transport (see also below regarding the place of supply), neither the supply of gas through the gas network nor the supply of electricity constitutes an intra-Community transfer or an intra-Community acquisition (sec. 1a.1., para. 1, sentence 7 of the German Administrative VAT Guidelines).

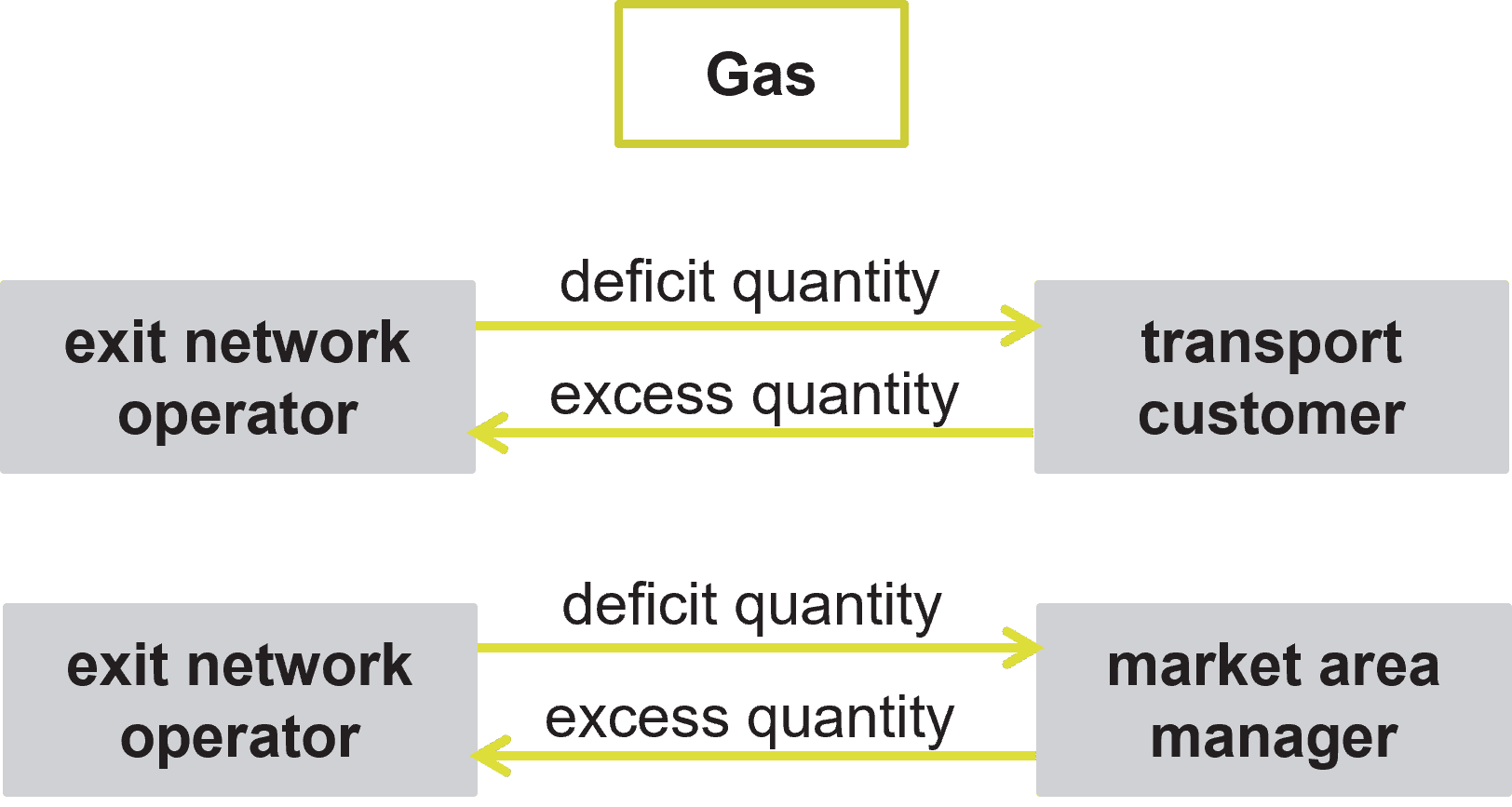

1.2 Supply of excess and deficit quantities

When balancing excess or deficit quantities with regard to electricity and gas supplies, the direction of supply must be taken into account.

Gas supplies

Excess or deficit quantities with regard to gas supplies are balanced between the exit network operator (Ausspeisenetzbetreiber) and the transport customer (Transportkunde) when the allocated quantity differs from the quantity actually delivered to the final consumer (sec. 25 German Gas Network Access Regulation – GasNZV). According to sec. 1.7., para. 5 of the German Administrative VAT Guidelines, a deficit quantity (allocation < actual withdrawal) constitutes a supply from the exit network operator to the transport customer. Conversely, in the case of an excess quantity (allocation > actual withdrawal), the transport customer supplies gas to the exit network operator. The same applies between the exit network operator and the market area manager (Marktgebietsverantwortlicher). The latter procures the necessary gas reserves for balancing excess and deficit quantities on the balancing energy market (Regelenergiemarkt) and either forwards them to or receives them from the exit network operator.

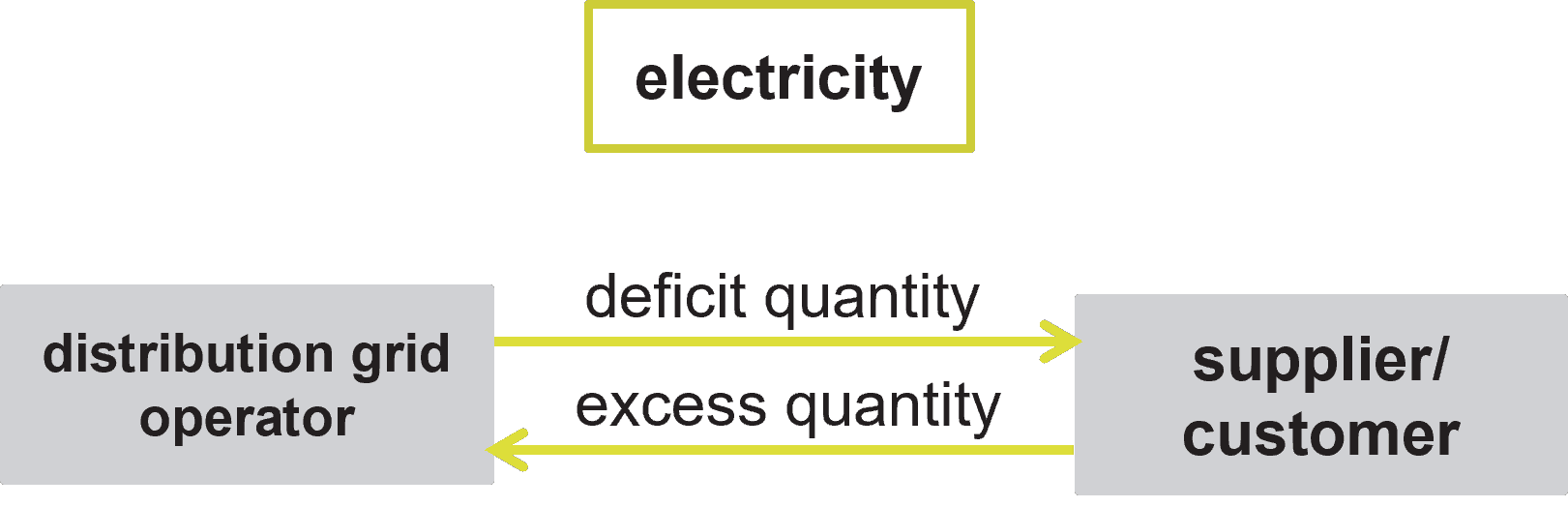

Electricity supplies

In the case of electricity supplies, excess or deficit quantities are also balanced between the distribution grid operator (Verteilnetzbetreiber) and the supplier or customer (sec. 13 Electricity Grid Access Regulation (StromNZV). From a VAT perspective, in the event of a deficit quantity, a supply is being made by the distribution grid operator to the supplier or customer. Conversely, in the case of an excess quantity, the supply is being made by the supplier or customer to the distribution network operator. (sec 1.7., para. 6 of the German Administrative VAT Guidelines)

1.3 Non-taxable supply in the case of direct consumption of electricity

In its letter dated March 31, 2025, the German Federal Ministry of Finance (BMF) adopted the view of the German Federal Fiscal Court (BFH) (judgment of November 29, 2022 – XI R 18/21, and May 11, 2023 – V R 22/21) and amended sec. 2.5. of the German Administrative VAT Guidelines accordingly: the direct consumption of electricity in cogeneration plants (CHP) eligible for subsidies does not constitute a supply. If the plant operator uses the generated electricity on a decentralized basis for its own consumption, no right to dispose of a tangible good is transferred to the grid operator. Consequently, neither a supply nor a return supply takes place between the plant operator and the grid operator. Even the payment of a CHP surcharge for electricity generated and consumed on a decentralized basis does not result in a taxable supply. Likewise, electricity offered and remunerated under a commercial-balance-sheet feed-in arrangement does not constitute a supply if the consumption occurs within a network that is not used for general supply and is not operated by a grid operator. If the plant operator supplies himself (known as customer system), this is irrelevant for VAT purposes.

See KMLZ VAT Newsletter 10/2025: A turnaround with need for action – new Federal Ministry of Finance’s letter on energy generation plants

2 What criteria determine the place of supply for energy?

The place of supply for gas supplied through the gas network, electricity, heat supplied via a heating network, and cooling via a cooling network is not determined by the general principles set out in sec. 3 para. 6-8 of the German VAT Act, but rather by the special provision in sec. 3g of the German VAT Act. In contrast, for the supply of bottled gas or the supply of gas by a tank truck, the place of supply is determined according to sec. 3 para. 6-8 of the German VAT Act, depending on whether the transaction constitutes a supply of goods with transportation or a local supply.

When applying the special provision of sec. 3g of the German VAT Act, paragraphs 1 and 2 require a distinction between supplies to a reseller and supplies to another purchaser (e.g. end consumer):

Reseller (as defined in sec. 3g.1., para. 2, 3 of the German Administrative VAT Guidelines: A taxable person whose main activity consists in acquiring and reselling the products of energy supplies listed in sec. 3g German VAT Act. A principal activity is assumed if at least 50% of the acquired quantity is resold. The taxable person’s own consumption must be of minor importance, meaning that no more than 5% may be used for their own needs. The preceding calendar year is decisive for determining reseller status.): With the reseller certificate (form template USt 1 TH), which is issued by the tax office either upon application or ex officio, the reseller can prove his reseller status to his suppliers. The certificate has indicative value but does not itself establish the application of the reverse charge mechanism. What is decisive is whether the reseller status exists objectively in accordance with sec. 3g of the German VAT Act. The certificate is generally valid for three years. Although the certificate itself is not a prerequisite for the application of the reverse charge mechanism, taxable persons should monitor its validity period and ensure that expired certificates are regularly reviewed and renewed in due time.

The place of supply is the place where the purchaser operates his business or, in the case of delivery to a fixed establishment, the location of respective establishment.Other purchasers (i.e. all persons who do not meet the criteria of a reseller. This typically includes end consumers):

In such cases, the place of supply is determined by the actual place of use or consumption. As a rule, the place of supply is therefore where the purchaser’s meter is located (see sec. 3g.1., para. 5, sentence 1 of the German Administrative VAT Guidelines).

3 Can an energy supply be exempt from VAT?

For energy supplies subject to the special place-of-supply rule under sec. 3g of the German VAT Act, VAT exemptions for exports pursuant to sec. 6 in conjunction with sec. 4 no. 1 lit. a of the German VAT Act or for intra-Community supplies pursuant to sec. 6a in conjunction with sec. 4 no. 1 lit. b of the German VAT Act do not apply. Due to the absence of transportion of goods, these exemption provisions are not relevant, and the respective supplies are subject to VAT.

In contrast, the importation of natural gas through the gas network or natural gas fed into the network or an upstream pipeline system from a gas tanker as well as the importation of electricity, heat, or cooling via heating or cooling networks is VAT exempt. This is based on the special provision in sec. 5 para. 1 no. 6 of the German VAT Act, under which such imports are VAT exempt.

4 Which VAT rate applies to the supply of energy?

As a general rule, the supply of energy is subject to the standard VAT rate of 19% in accordance with sec. 12 para. 1 of the German VAT Act. However, in response to the energy crisis, the German Federal Parliament enacted a temporary reduction of the VAT rate to 7% for supplies of gas through the gas network and for supplies of heat via heating networks, applicable from October 1, 2022, to March 31, 2024 (Act on the Temporary Reduction of the VAT Rate on Gas Supplies through the Gas Network – Federal Law Gazette I 2022 No. 38 of October 25, 2022, p. 1743; Letter of the German Federal Ministry of Finance dated October 25, 2022). In addition, reduced VAT rates apply in special scenarios, such as for photovoltaic systems.

In addition to the reduction of the VAT rate, the so-called energy price brake was introduced in this context. Its relief effect applied retroactively from January 1st, 2023 and was implemented through the billing of energy suppliers. It expired on December 31st, 2023. The tax authorities have not yet commented on its VAT treatment. However, according to prevailing opinions in the literature, it constitutes a consideration from a third party for VAT purposes. This means that the energy supply company remains liable for VAT on the entire supply of energy, even if part of the consideration is covered by the government.

4.1 VAT rate reduction due to the energy crisis

According to the German tax authorities (letter of the (German) Federal Ministry of Finance dated October 25, 2022, paras. 5-9), the VAT rate reduction does not only apply to gas supplies through the gas network but also to supplies delivered by tank trucks to the recipient for the purpose of heat generation. In addition, the reduced VAT rate applies to the installation of a household gas connection, the settlement of excess or deficit quantities between the market area manager, the exit network operator and the transport customer, as well as to heat supplies via heating networks.

Timewise, all supplies carried out during the period from October 1, 2022, to March 31, 2024, are subject to the reduced VAT rate. This reduced rate must also be applied in cases of cash accounting [scheme] (e.g. for down payments, payments on account, or advance payments) even if VAT became chargeable before October 1, 2022, but the associated service was or will be carried out during the reduced-rate period.

4.2 Reduced VAT rate for special cases

The standard VAT rate does not apply when electricity is supplied in connection with the short-term rental of residential or sleeping accommodations or of camping areas, and the supply directly serves the accommodation/rental. In such cases, a reduced VAT rate applies. According to sec. 12 para. 2 no. 11 of the German VAT Act, the applicable VAT rate is only 7%. This applies even if a separate charge is paid for the electricity supply (see sec. 12.16., paras. 4 and 7, sentence 4 of the German Administrative VAT Guidelines).

4.3 Zero VAT rate for certain photovoltaic systems

For the supply of solar panels to the operator of a photovoltaic system – including essential components for the operation of the system and storage units – the VAT is reduced to 0% in accordance with sec. 12 para. 3 of the German VAT Act. This provision was incorporated into the VAT Act effective January 1, 2023. The German Federal Ministry of Finance has already issued several statements on this matter, including the Federal Ministry of Finance’s letters dated February 27, 2023, and November 30, 2023.

KMLZ VAT Newsletter 39/2022: Annual Tax Act 2022 (draft): Zero VAT rate on photovoltaic systems

KMLZ VAT Newsletter 14/2023: Zero VAT rate on photovoltaic systems - The Ministry of Finance’s letter comes with changes

KMLZ VAT Newsletter 49/2023: Zero VAT rate for the supply of photovoltaic systems: Ministry of Finance publishes further circular letter

5 What applies with respect to the tax point of the supply of energy?

For supplies, VAT arises pursuant to sec. 13 para. 1 no. 1 lit. a of the German VAT Act on the expiry of the preliminary VAT return period in which the transactions has been carried out. In the case of supplies, this generally corresponds to the point in time when the right to dispose of the supplied item is transferred. However, with regard to energy supplies, the following specific aspects must be taken into account concerning the timing the supply is carried out:

Relevance of the meter reading period

For supplies of electricity, gas, heat, cold, and water, the meter reading period is in general decisive. These supplies are only considered to have been carried out once the respective meter reading period has expired (see sec. 13.1., para. 2, sentence 4 of the German Administrative VAT Guidelines). At that point, the corresponding VAT incurs.

A distinction must be made between SLP customers (standard load profile) and RLM customers (registering load measurement):

SLP customers – typically households and small business customers with an annual electricity consumption below 100,000 kWh or gas consumption below 1.5 million kWh – make monthly advance payments based on a forecast consumption pattern (standard load profile). The actual billing usually takes place once a year based on the actual annual consumption measured at the end of the annual reading period. For VAT purposes, the end of the annual reading period is therefore decisive.

RLM customers – generally large consumers with higher energy demand – have meters that record consumption in 15-minute intervals and can be read remotely. They receive monthly invoices based on the measured load profiles. Here too, the end of the respective (monthly) reading period is decisive for the VAT tax point.

The VAT tax point is also decisive for determining the applicable VAT rate. For this purpose, the end of the meter reading period is relevant. It is irrelevant which VAT rate applied at the beginning or during the meter reading period. As a result, the entire consumption during a meter reading period is generally subject to one single VAT rate.

Gas supplies in the B2B sector

In the B2B sector of the gas business, contracts in consideration of the so called “gas month” are often agreed upon. This results in monthly partial supplies within the meaning of sec. 13 para. 1 no. 1 lit. a sentence 3 of the German VAT Act. According to sec. 23 para. 1 sentence 2 of the Gas Network Access Ordinance (GasNZV), the "gas day" traditionally ends at 6:00 a.m. on the following calendar day. If the supplier and the recipient have agreed upon settling accounts based on the gas day, the billing for a calendar month is carried out on the 1st of the following month. Only at that point is the respective supply considered to have been carried out. Consequently, the VAT incurs only for that preliminary VAT return period.

6 Who is liable for VAT in the case of energy supplies?

For the energy supplies listed below, the liability for VAT is reversed in accordance with sec. 13b para. 2 no. 5 of the German VAT Act, meaning that the recipient of the supply becomes liable for VAT:

In the case of supplies of gas through the gas network, electricity, as well as heat and cold via heating or cooling networks, the VAT liability is reversed if a taxable person resident abroad supplies to another business under the conditions set out in sec. 3g of the German VAT Act. (sec. 13b.3a. para. 1 of the German Administrative VAT Guidelines)

Moreover, the reverse charge mechanism also applies to gas supplies through the gas network if a taxable person established in Germany supplies gas to a reseller. In the case of electricity supplies by a taxable person established in Germany, the VAT liability is only reversed if both the supplier and the recipient are resellers. (sec. 13b.3a. para. 2 of the German Administrative VAT Guidelines)

It should also be noted that supplies of water and energy do not constitute construction services within the meaning of sec. 13b para. 2 sentence 1 no. 4 of the German VAT Act. Therefore, reverse charge based on this provision is not applicable.

7 What applies to the supply of energy and other measures for grid operators and plant operators?

Grid operators and plant operators must also observe certain specific provisions:

Energy supply in the form of control area and balancing group compensation

If a transmission system operator supplies energy as part of the known as balancing group and control area compensation, this does not constitute an independent supply of goods. Instead, it qualifies as a supply of service, specifically for maintaining voltage and frequency. Furthermore, it is considered a supply of service and not a supply of goods when an energy supplier transfers excess energy capacities to a customer at a negative price (i.e., the energy is no longer saleable at a positive price and is therefore transferred with an additional payment).

Supply of service due to the provision of electricity at negative prices Redispatch 2.0 measures

Further VAT-related specific provisions apply when grid operators (connection grid operators, transmission system operators, and distribution system operators) must take measures under Redispatch 2.0 (see German Federal Ministry of Finance’s letter dated 26 August 2024). When congestion is imminent, grid operators are required to intervene in the generation output of power plants in order to protect grid sections from overloading.See KMLZ VAT Newsletter 42/2024: VAT perspective of Power Plant Redispatch 2.0 and its compensation

Determination of the taxable amount for withdrawal of heat as a supply without consideration

If heat is withdrawn from a cogeneration unit or a biogas plant as a supply carried out free of charge within the meaning of sec 3 para. 1b sentence 1 no. 1 of the German VAT Act, the taxable amount is determined in accordance with sec. 10 para. 4 no. 1 of the German VAT Act. As a rule, the decisive factor is the (fictitious) purchase price of a similar item. If a (fictitious) purchase price cannot be determined, the calculation must be based on the cost price (including production, acquisition and financing costs). In cases of both remunerated supplies and supplies without consideration of heat, these costs must be allocated between electricity and heat. According to sec. 2.5. para. 16 sentences 6-10 of the German Administrative VAT Guidelines, the allocation must generally be made using the market value method (and not the energy-allocation-method based on the ratio of produced quantities of electrical and thermal energy in kWh). The average heating price may not be used instead of the actual cost price.See KMLZ VAT Newsletter 10/2025: A turnaround with need for action – new Federal Ministry of Finance’s letter on energy generation plants

8. Operation of Battery Storage Systems

The operation of battery storage systems (e.g., stationary electricity storage units) is becoming increasingly important for the energy sector. This is not least due to the continued expansion of renewable energy sources. The correct VAT treatment largely depends on whether the owner of the battery storage facility actually has power of disposal over the stored electricity. In this respect, it is important that the owner of the storage facility drafts civil law contracts as unambiguously as possible, e.g., the contract with a (management) service provider. Civil law can influence whether the parties involved intend to carry out and actually perform a supply of energy, or whether the transaction merely constitutes a supply of services.